In 2007, CEO Rick Kent founded Merit Financial Advisors in Atlanta as a hybrid registered investment advisor. He has since grown it into a $10 billion business with more than 40 offices across the United States, with support from Wealth Partners Capital Group and a group of strategic investors led by HGGC. This month, Merit launched a new 1099 alliance model.

Merit has attracted many talented people along the way, including Brian Andrew, who recently joined the firm from Johnson Financial Group as chief investment officer. Andrew is tasked with managing the firm’s investment arm and asset allocation decisions. He will also play a key role in integrating new partner companies acquired by Merit.

Wealth Management Network I recently interviewed Andrew and he introduced one of Merit’s core model portfolios.

Wealth Management Network I recently interviewed Andrew and he introduced one of Merit’s core model portfolios.

The following content has been edited for length and clarity.

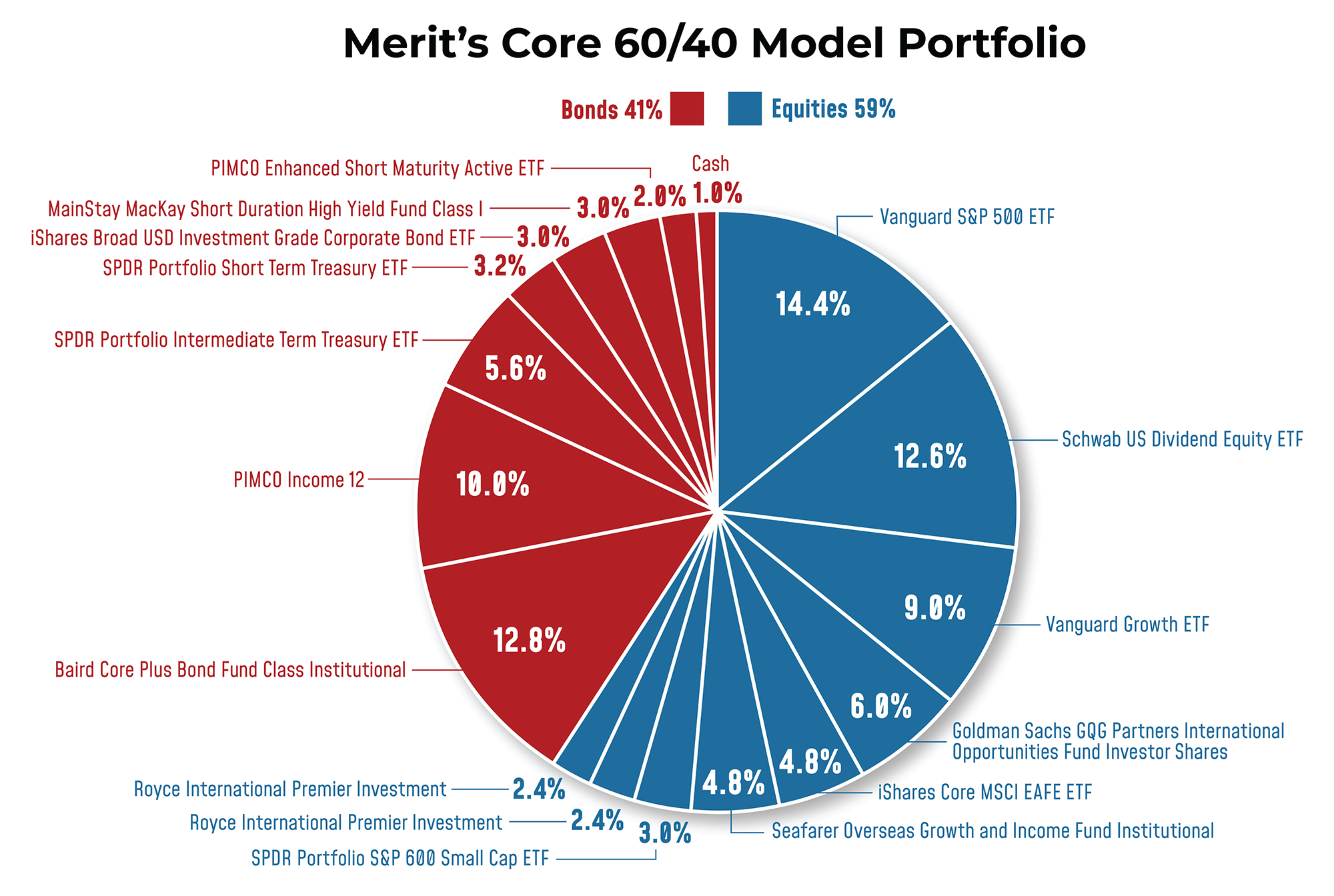

WealthManagement.com: What is included in your model portfolio?

Brian Andrew: There are both passive and active types in the investment portfolio, with the passive type mainly being ETF positions. We are very cost-conscious when it comes to building portfolios for our clients. Therefore, holding ETF exposure helps reduce costs.

Second, we are tactical in nature, which means we are interested in making changes in the near term. Changing ETF positions is easier. Obviously, they are more sensitive to market changes, which makes our tactical positioning more flexible. So this is the main reason to be exposed to both passive and active.

I would say given the size of Merit, we have all ETF model portfolios. This core product portfolio we’re talking about here is the one most used across the organization. However, for clients and advisors who are super cost-conscious and really just want indexing, our ETF portfolios follow the same strategic and tactical positioning as our core portfolios.

This core model is about 60/40. We do maintain an average cash position of about 2%, and we don’t really make what we call large strategic asset allocation bets, where we own 50%, then we’re 75%, then we’re 25%. We might be overweight or underweight stocks by 2 or 3 percentage points, but not by much.

Tactical changes do occur within asset classes. If you think about large-cap stocks, relative to smaller growth, relative to value, or high credit quality, low credit quality, those kinds of things. On the bond side of the portfolio, we’re worried about interest rate sensitivity; we’re worried about sector allocation. We worry about credit quality.

We did put some thought into the shape of the yield curve. Today, the curve is still a short to long reversal, so we believe there is an opportunity in the middle part of the curve and we will take advantage of that, while perhaps at other times we will be more short and long. So that’s a positioning change that we’re going to make on the bond side of the portfolio. This is actually another good example of how ETFs can do this more easily than active core bond managers.

WM: What is the weighting of domestic versus international in the equity allocation?

Bachelor: Our benchmark is the MSCI ACWI Index. The allocation to international and emerging markets is higher in our benchmark compared to using a domestic-international hybrid benchmark. Therefore, compared with ACWI, we reduce our holdings in international emerging markets by about 10%. We allocate less than one-third of our equity portion to international companies.

People have long said that international stocks are attractively valued, but this remains the case. There are still some meaningful opportunities there. But when you look at the portfolio, there’s more active exposure because we think those active managers are better positioned.

The current valuations are there for a reason. The European economy does not look like it will recover like the US. Weakness in China also leads to weakness across Asia. Many European companies, especially manufacturers, are export-oriented. That’s why valuations are where they are. But I think there are some opportunities, if you will, to have additional exposure at this time.

We are also slightly overweight small and mid-cap stocks, again due to valuation reasons. Small-cap stocks, in particular, have become extremely unpopular. We all know that if you look at the S&P 500 and remove the top 7 to 10 stocks, you eliminate over 75% of the performance.

If you take the valuation of the Russell 2000 Index as an example, it is trading at a relatively low level compared to the growth of the Russell 1000 Index. I would say that we are probably among those small-cap managers that don’t need a big cyclical recovery to win. I don’t think our view is that economic growth will grow from 2% to 5% in 2024. I think we’ll be lucky to hit 2% this year. But we still believe there are more opportunities in this part of the market from a valuation perspective.

WM: Have you made any significant allocation changes in the last six months or so?

Bachelor: The overweighting of small and mid-cap stocks was a change that occurred at the end of last year.

The other change is more on the fixed income side of the portfolio, where we have shorter duration. Our benchmark is the Bloomberg Aggregate Bond Index, which has a maturity of approximately six years. We are well below four years and currently just over four years. Therefore, the increase in duration comes from the recovery in yields between the third and fourth quarters. But we are still short.

We have also adjusted our active manager structure to improve credit quality. Our view is that we haven’t seen all the weaknesses that we’re going to see. For example, historically, the yield differential between Treasuries and corporates has remained very small. We believe it makes sense to own a portfolio with higher credit quality relative to the benchmark. The original high-yield bets have largely disappeared, and the average credit quality of our entire portfolio has improved.

WM: You mentioned that you hold 2% in cash. Why hold cash?

Bachelor: I wish I could tell you that this is backed by science, but two things: One is, if I could run it at zero, I would, but we know there are always distributions or fees, like investment management fees. Folder. To ensure clients are fully invested and don’t incur fees for overdrafts, we keep a little cash on hand. Second, Merit has done a great job improving the way we use trading technology, so that number has gone down a bit. I hope we can get back to the 1% level. Until we improve the way we trade and the technology we use, this number may be closer to 5%.

WM: Are you investing that cash into any specific structure?

Bachelor: For clients that we know can do something with their cash, we may switch them from money market funds to ultra-short funds because their duration will be closer to one year as opposed to the days of a 30-year money market fund. As long as you can have cash, you can get a pretty good rate of return, and people can tolerate the marginal fluctuations brought by ultra-short-term funds. That happens almost every customer to customer, not necessarily in the model, but we have that resilience built into the way we do things.

WM: Are you allocated to private investments and alternatives? If so, what parts did you like?

Bachelor: The organization has been using liquid alternatives for some time and has a number of model portfolios using liquid alternatives that advisors can use as a playbook for clients interested in alternative allocations. This is actually the result of a long-standing low-yield environment. This is a way for clients to generate income using alternatives rather than traditional fixed income.

Within this scope, investments can be made through liquid alternative funds in real assets such as private equity, private credit and infrastructure or commodities. People can own it and fund it from the income or equity portion of their portfolio, depending on their return goals.

On the private placement side, we are evaluating external partners. We may first enter into a partnership with a larger national firm (such as CAIS or iCapital) that can provide us with private placement financing opportunities. This will ultimately lead to us creating our own white label fund, in which we select the investments we ultimately make and then make them available to clients who are able to invest in alternative investments due to their accredited or qualified status.

We don’t need partners to help us get funding. What’s more important is how they help us from a technical perspective through subscription documentation, research and due diligence, and then help us think about how to integrate these funds into the client’s strategy.

WM: What makes your portfolio unique?

Bachelor: I mentioned earlier the idea of using both passive and active in the same model portfolio, with all passives available.

Another thing is that understanding an active fund manager’s performance cycle is just as important as understanding how they manage their money. I mean, people often talk about a tactical shift between factors like size or growth versus factors like value or dividend yield. If you look at a specific segment like small-cap growth stocks, you’ll see that not every small-cap growth fund manager is the same, and they have different performance cycles throughout the market cycle. Some are more or less competitive depending on the underlying economic theme. One small-cap manager’s catalyst isn’t another manager’s.

One of the things that sets us apart is understanding not just the long-term track record, but understanding the team, their approach to stock picking, and how it works at different stages of the market cycle and based on what the underlying economic environment looks like. Because then you can not only strategize, move in and out of small scale or large scale, but you can also compare one manager to another based on how they perform relative to their peers. This allows you to take advantage when a manager performs significantly better than other managers; you can more easily sell winning stocks and buy losing ones because you know the strategy will work over time.