Greenvalds

Jerky is no longer as respected as it once was, not even in Los Angeles, which is why they had to build Vegas. ——Ross MacDonald

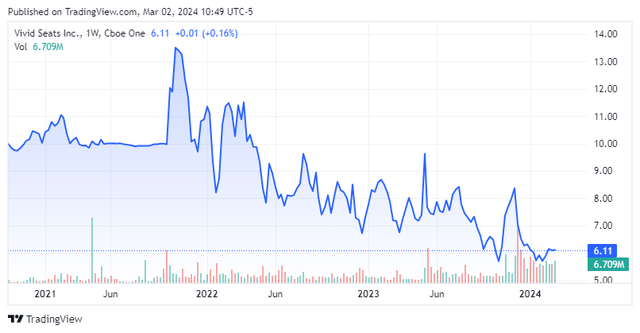

Exchange shares online Vivid Seating Company (NASDAQ: SEAT) Hits all-time intraday low $5.54 On February 2, 2024, private equity faces a huge threat. The stock has since rebounded about 10%. The company’s acquisitions of Vegas.com and Wavedash expand its total addressable market by more than 50% in 2023 and will increase revenue and adjusted profits. EBITDA in 2024. With 76.2 million private equity shares still outstanding, but previously bloated valuation metrics now less severe, this failed IPO deserves a closer look. Below is the analysis/recommendations.

Seeking Alpha

Company Profile

Vivid Seats Inc. is a Chicago-based online ticket marketplace that coordinates customer payments and ticket delivery through its website and app.It also provides loyalty programming, ticket insurance and fantasy sports products. Vivid was founded in 2001 and went public in 2021 after being merged into the special purpose acquisition company (SPAC) Horizon Acquisition Corporation, first trading at $13.14 per share. The stock currently trades at just over $6 per share, equating to a market capitalization of just under $1.3 billion.

The company consists of two classes of shares. The 133.7 million publicly traded Class A shares confer financial benefits and one vote per share. The 76.2 million privately held Class B shares are held primarily by private equity firms, specifically Vista Equity Partners and GTCR. They confer no financial interest, have one vote per share, and are convertible into Class A shares.

business model

Vivid divides its activities into agents (marketplace) and principals (resale).

Marketplace provides a trading platform for ticket buyers and sellers, and the company charges 10% of the total order value (GOV) from sellers and service and delivery fees from buyers. In addition to these revenue streams, Vivid sells buyer’s insurance through third-party providers, generates revenue through its platform as a private-label product, and makes additional contributions to its revenue through daily fantasy sports products. For the first nine months of 2023 (YTD23), the segment’s contribution margin was US$166.4 million and revenue was US$430.1 million, an increase of 20% and 16% from YTD22 (respectively), mainly including concerts (56%) and sports (33% ), and theater (11%) ticket sales. (Contribution margin is defined as revenue minus cost of revenue and marketing and selling expenses.)

Resale primarily involves Vivid acquiring tickets and selling them on secondary ticket markets, including its own market. Its profit contribution from the beginning of 2020 is US$20.4 million and revenue is US$84.5 million, an increase of 36% and 31% respectively from the year to date in 2020.

These segments are supported by what management describes as the most generous loyalty program in the space, driving repeat business. Launched in 2019, the service features a buy-10-ticket-get-1-free promotion aimed at increasing brand awareness, which was below 10% when the company went public in 2021, the lowest among the top five ticket brokers. The proportion of repeat customer orders in total orders will grow from 47% in 2018 to 56% in 2022.

Growth through acquisitions

In addition to leveraging sales and marketing to grow its brand organically, Vivid has made multiple transactions since going public to expand its total addressable market, the most significant of which was the acquisition of Vegas.com in November 2023. Sin City’s shows, hotels, vacation packages, tours, attractions, dining and nightlife received $243.8 million in consideration, including $153.6 in cash and approximately 15.6 million SEAT shares. In return, Vivid gets access to a total addressable market (TAM) worth $6 billion, essentially its oasis in the $20 billion North American opportunity (2023). Coupled with the $74.3 million acquisition of Japan’s leading online ticket marketplace Wavedash in September 2023, Vivid’s TAM grew by more than 50% in fiscal 2023 to approximately $21 billion.

November company introduction meeting

market

The TAM expansion will help the company compete with the likes of StubHub, Live Country (LYV) The global market for Ticketmaster and Seat Geek is expected to reach $63 billion by 2024. To put Vivid’s market dominance into perspective, in January 2022 it sold its 100 millionth ticket since 2001. Live Nation sold 550 million tickets in 2022 through Ticketmaster and other related websites and apps, retail stores and call centers.

share price performance

Vivid, which survived a pandemic with no one attending concerts or sporting events, went public just as the world was starting to return to stadiums and theaters and just before interest rates spiked to market revaluation levels. Generating Adj. Fiscal 2020 EBITDA of negative $80.2 million on revenue of $35.1 million, the company rebounded to produce fiscal 2021 adjusted EBITDA. EBITDA was positive $109.9 million on revenue of $443 million. However, at its opening price of $13.14, Vivid is valued at EV/FY21 adjusted valuation. EBITDA is 23.3. The market remains satisfied with management’s original adjusted forecast for fiscal 2022. EBITDA was $112.5 million on revenue of $530 million, which the company beat slightly on an adjusted basis. EBITDA was $113.3 million and revenue was $600.3 million.

However, as part of the IPO, Vivid received $225 million in PIPE investment from third-party investors, including Draft King(DKNG)One year after the Horizon SPAC merger closed, the company had the option to sell its shares at $9.77. As markets tend to do, private equity dynamics, a significant glut, and rising valuations kept SEAT shares trading in a tight trading range between $7 and $9 from June 2022 to August 2023. $0.36 per share (GAAP) in fiscal 2022, $0.43 per share (GAAP) year-to-date in 2023, and an initial adjusted $0.43 per share in fiscal 2023. EBITDA forecast was $112.5 million (which has since been raised to $139 million to reflect its two acquisitions and a slightly better-than-expected business), but EV/Adj remains expensive. EBITDA fundamentals given its moderate growth prospects. As a result, as private equity looks to exit, potential buyers have been waiting for “selling shareholders” secondary assets as an opportunity to invest at slightly depressed prices.

The most recent such event occurred in December 2023, when the private equity firm sold 23.575 million shares at $6.50 per share. However, realizing that 76.2 million shares are still for sale at some point in the future makes it hard to get excited about investing in Vivid. It should also be noted that the principals of Vegas.com have filed to sell more than half of the shares (7.8 million shares) they received as consideration for the transaction. As a result, Vivid’s stock price hit an all-time intraday low of $5.54 per share on February 2, 2024.

3Q23 Financials

Even its Q3’23 financial report on November 7, 2023, which simultaneously acquired Vegas.com and made early optimistic forecasts for fiscal 2024 prospects, did little to change people’s sentiment. The company reported net income of $0.07 per share (GAAP) and adjusted net income of $0.07 per share. EBITDA was $33.4 million, revenue was $188.1 million, earnings per share (GAAP) were $0.09, and adjusted earnings per share were $0.09. EBITDA for the third quarter of 2022 was $28.3 million and revenue was $156.8 million, a decrease of 15% (in U.S. dollar terms) and an increase of 18% and 20%, respectively. In addition, the market’s total order value (GOV) was US$998.9 million, an increase of 28% from US$781.8 million in the same period last year.

November company introduction meeting

With the announcement of the Vegas.com acquisition, management took the additional step of providing a preliminary outlook for fiscal 2024, which includes an adjusted outlook for fiscal 2024. EBITDA was $175 million, revenue was $825 million, and market GOV was $4.35 billion. Vegas.com’s contribution to the revenue outlook will be in the range of $82.5 million to $100 million. All forecasts are based on the midpoint of the range.

November company introduction meeting

Balance Sheet and Analyst Comments

The cash portion of the Vegas.com deal comes from Vivid’s strong balance sheet, which holds $105 million in assets versus $274 million in debt, resulting in a post-acquisition net leverage ratio of 1.2 (as of 2023). Additionally, Vivid has access to an undrawn credit facility of $100 million. The company repurchased $40 million of stock in 2022 and then purchased 2 million shares as part of a secondary offering to selling shareholders in December 2023. Vivid does not pay dividends.

November company introduction meeting

Despite the pending private equity investment, Wall Street has mixed views on the company’s future, with 3 Buy and Outperform ratings issued so far in 2024, compared to 2 Hold ratings. expected The company expects fiscal 2023 earnings of $0.46 per share (GAAP) on revenue of $698.6 million and fiscal 2024 earnings of $0.42 per share (GAAP) on revenue of $822.4 million, reflecting Vegas .com joining.

judgment

It’s hard to find a bottom for a stock that just hit an all-time low, but the decline in stock price combined with the Vegas.com acquisition makes Vivid attractive on the EV/Adj side. For the first time in its short history as a public company, the EBITDA basis is trading at just below 11 on an adjusted basis for fiscal 2023. Adjusted EBITDA and EBITDA of 8.5% in fiscal 2024. Additionally, it currently trades for FY2024 sales at 1.55, while its FY2024 GAAP EPS ratio is just 14.5 — both reasonable factors given its future prospects. As with the economy, the private equity glut remains a concern, but with solid cash generation and the best valuation metrics since going public, this failure could be a win-win if investors are willing to wait out the private equity glut. IPO is worthy of a small “observation”. . Fourth-quarter results will also be released later next week. We’ll probably look back at this story sometime later this year.

Las Vegas is the savage center of the American dream. ——Hunter Thompson