Andrei Yalansky

As we all know, you get what you pay for, and good stocks are often expensive.That’s why in our first article TriplePoint Venture Capital Growth (NYSE:TPVG), we are confused by investors Additional fees are being paid for this Business Development Company (BDC). Maybe the reason is the dividend yield. The high dividend yield on common stocks is certainly a huge draw. However, a determined BDC cannot achieve this goal through a stable and growing net worth, while TPVG aims to achieve this goal through a declining net worth.

Well, with all the euphoria of the past three months, that didn’t seem to matter. But maybe it’s still possible.

Q4 2023

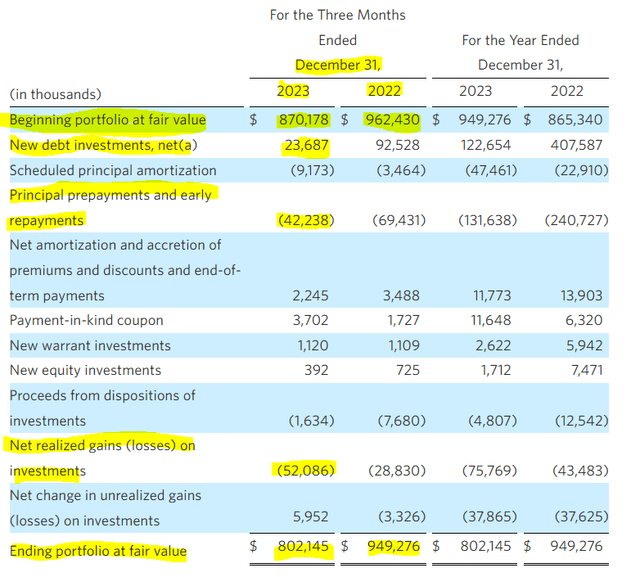

It’s been a tough quarter (linked 10-K) for TriplePoint Venture Growth, which posted a loss of $52 million.Combined with principal repayment of the underlying company and a small The portfolio value fell by approximately $68 million last quarter as new investments increased.

TPVG Fourth Quarter 2023 Results

You can see the significant change in the portfolio’s fair value at the end of the period from December 2022 to December 2023 in the same chart.

We recognized a net realized loss on investments of $75.8 million for the year ended December 31, 2023, primarily due to write-offs of investments in Hi.Q, Inc., Demain ES (d/b/a Luko), Untitled Labs , Inc., Mystery Tackle Box, Inc. (d/b/a Catch Co.) and VanMoof Global Holding BV

Source: TPVG fourth quarter 2023 results.

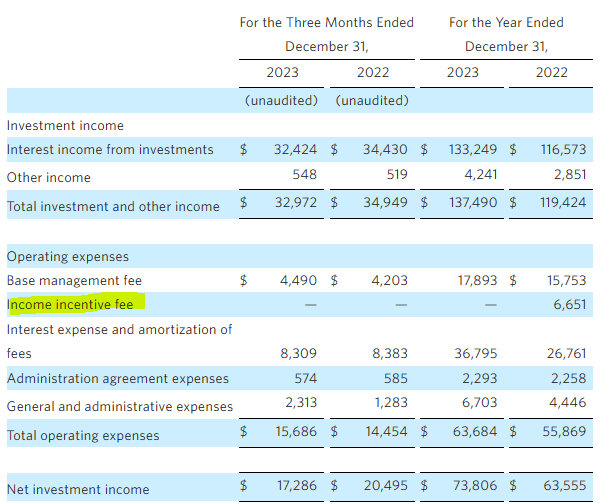

However, the company did report net investment income of $0.47 and stuck to its $0.40 dividend payout ratio. Taking into account pre-market action, you’re now looking at a yield of 16%. Do you bite?

Weakness

Notably, TPVG has been able to maintain its dividend thanks to the incentive fee exemption. If you had something like a normalized level, it would be difficult to get NII higher than its current dividend yield.

TPVG Fourth Quarter 2023 Results

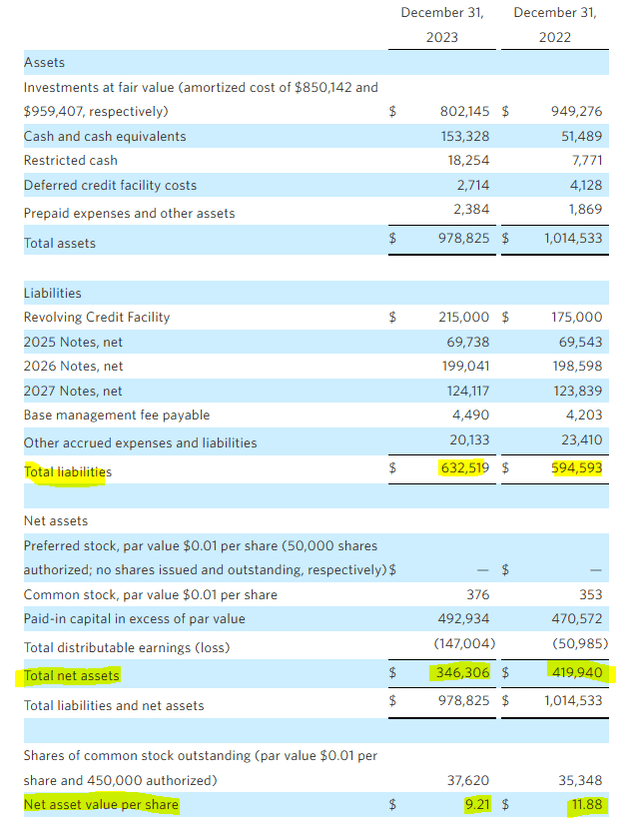

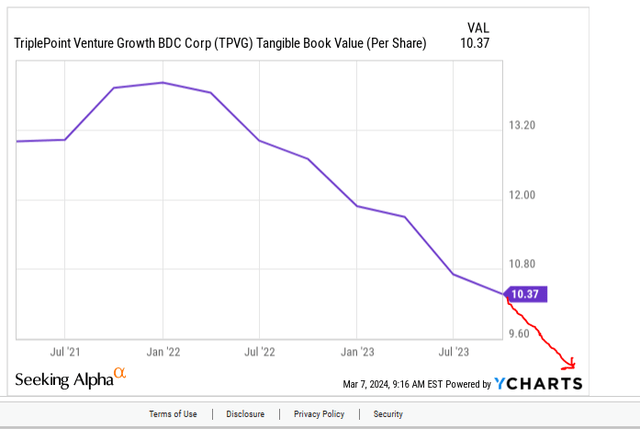

But dividend chasers may see this as a positive, as the company appears to be looking for investors. Well, maybe. But without incentive fees, you can expect top talent to eventually leave the company, leaving you with bigger problems in the long run. But let’s put that aside for a moment. The bigger problem is that the NAV fell from $11.88 to $9.21 in one year.

TPVG Fourth Quarter 2023 Results

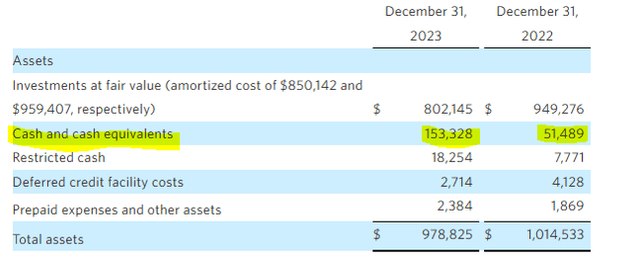

At the same time, leverage has also increased. Some of the increase in leverage is a bit misleading, as the company has also increased the amount of cash it has on hand.

TPVG Fourth Quarter 2023 Results

The incremental net leverage is therefore much lower. But some commitments may even cause net leverage to rise.

The Company’s total unfunded commitments as of December 31, 2023 were $118.1 million, of which $29.2 million is contingent on the portfolio companies achieving certain milestones. Of the $118.1 million in unfunded commitments, $86.7 million is due in 2024 and $31.4 million is due in 2025 if not drawn before maturity. Because these commitments may expire without being drawn, unfunded commitments do not necessarily represent the Company’s future cash needs or future earnings assets.

Source: TPVG Fourth Quarter 2023 Results.

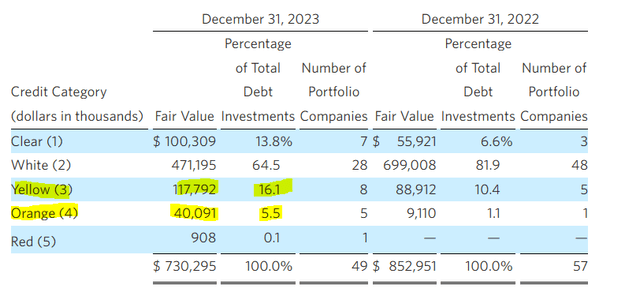

TPVG still has 21.6% of its portfolio marked as “yellow” and “orange.” Last year, our ratio was 11.5%.

TPVG Fourth Quarter 2023 Results

That figure stood at about $98 million at the end of 2022, with TPVG losing $75.6 million in the last 12 months. So after these losses, it’s a bit shocking that the yellow and orange categories represent 21.6% of the portfolio value. What’s even more interesting, and what we think is strange, is that the “red” remains barely observable during this time.

Appearance

We must remind investors that current market conditions are the “most accommodative” in terms of credit tightening. Keep this in mind when you read what the company has to say about its investments.

Non-traditional investors and others in growth markets have paused or stayed on the sidelines. This change also affects our growth-stage companies, many of which are planning an IPO or potential acquisition within approximately one to three years of their last funding round.

Given the downturn in the market, our priority remains closely managing our portfolio. Our team remains in close contact with our company and its venture investors while continuing to work on credit issues. Given the challenging financing environment for venture growth companies, for some we believe valuations and internal financing potential will continue to come under pressure. Some companies are further reducing cash burn and getting on the path to profitability.

Source: TPVG 2023 Q4 Conference Call Transcript.

We hate to think what would happen in a real recession if these companies were in trouble today. TPVG also used its ATM program to sell some stakes, which got at least one analyst a little excited.

Casey Alexander

Yes. I just have one question. How could it possibly be appropriate to sell 1.5 million shares to the market via an ATM scheme when you know you are about to report a significant loss this quarter and the net worth presented to shareholders will be significantly lower?

Sahar Srivastava

Yes. Kathy, this is Sahar. I want this.Therefore, the ATM machine is an independent program, so it operates according to our settings. (unclear).

Casey Alexander

Do you have the ability to shut it down?

Sahar Srivastava

Yes, and then as we say, as we learn or understand what’s going on, we adjust and act accordingly.

Source: TPVG 2023 Q4 Conference Call Transcript.

The company currently has a BBB rating from DBRS with a negative watch, something we will continue to monitor.

TPVG Fourth Quarter 2023 Results

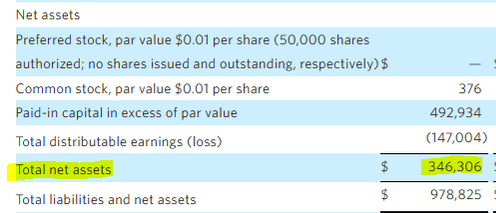

As we mentioned before, this equates to $157.88 million in total assets, or about 21.6%. But this figure represents 45.5% of net asset value.

TPVG Fourth Quarter 2023 Results

Do you want to solve this problem?

As of December 31, 2023, we had investments in five portfolio companies on a non-accrual basis with total cost and fair value of $41.7 million and $29.0 million, respectively.

Source: TPVG fourth quarter 2023 results.

Additionally, approximately 11% of the portfolio is paid out in kind or PIK, which is not very useful for the cash dividends TPVG needs to pay.

judgment

Over the past three years, TPVG has had the largest percentage decline in NAV among the companies we track in this industry. Morning coffee isn’t over yet here at YCharts, so we had to give you an update on what’s going on this season.

YCharts and author editing

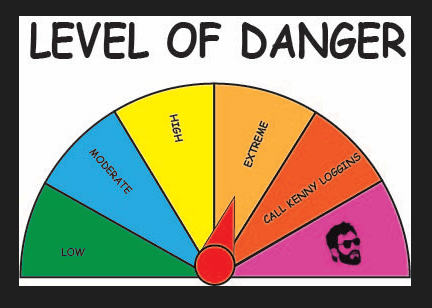

If you’re priced at 30-40% below NAV, we’ll stand on the sidelines and say, it’s probably already priced. But even after a 10% pre-market discount, it still trades above NAV. According to our proprietary Kenny Loggins Scale, TPVG is in danger of an “extreme” level of dividend cuts.

Author scale

The rating implies a 50-75% chance of a dividend cut over the next 12 months. Please note the 12 month time frame. It may take time to play out. The last time we used this rating scale, the dividend was cut within 12 days. If we had to guess, we think it will be cut within two quarters. We rate it a Sell and expect an upgrade following adjustments to pricing and dividends.

Please note that this is not financial advice. It looks like it, sounds like it, but surprisingly, it’s not. Investors should conduct their own due diligence and consult with professionals who understand their objectives and limitations.