Klaus Vedfelt/DigitalVision via Getty Images

While there are many publicly traded BDCs for investors to choose from, only a handful focus on lending to venture capital and post-growth companies.one of the largest and Arguably one of the best is Hercules Capital (high temperature gas chromatography). Others include TriplePoint Venture Growth (TPVG) and Trinity Capital (TRIN), is a relatively new entrant into the publicly traded BDC space. The latest in the group is Runway Growth Finance Corp (Nasdaq: RWAY), the subject of this article.

Who is Podium Growth Financial?

According to the company websiteRunway provides financing to later-stage and growth companies seeking alternative lending options.

Runway Growth Finance Corp. is a growth specialty finance company focused on providing flexible capital solutions to late-stage and growth companies seeking alternatives to equity financing.Our mission is to support Passionate entrepreneurs build innovative businesses. The company provides capital to companies looking to fund growth with minimal dilution – in turn, Runway Growth Finance seeks to generate favorable risk-adjusted returns for its shareholders.

Runway was founded in 2015 David Spren, a venture capitalist, is currently on medical leave. The company went public in October 2021. As of 12/31/23, the company’s total investment portfolio was valued at just over $1 billion, including $978 million in term loans, over 99% of which were senior secured first lien investments. Since inception, the firm has $2.5B in committed capital across 77 companies.

Fourth Quarter 2023 Results

RWAY reported Q4 2023 earnings yesterday (March 7), and investors weren’t happy with the results, sending the stock price plummeting -14% (as I wrote this on March 8). In my opinion, this is a buying opportunity for RWAY investors because the market punished RWAY investors. The stock reported a bad quarter, likely largely due to a sharp decline in NAV from $14.08 at the end of the third quarter to $13.50 at the end of the fourth quarter. Tom Ray Terman.

The decrease in net worth was primarily due to an unrealized loss of $7.7 million on our CareCloud preferred stock, which we elected to hold because we see opportunities for future stock appreciation, and a $17.0 million realized loss on our preferred stock. Debt investing with Pivot3. $6.4 million of this amount was reflected as unrealized losses in our third quarter 2023 financial statements.

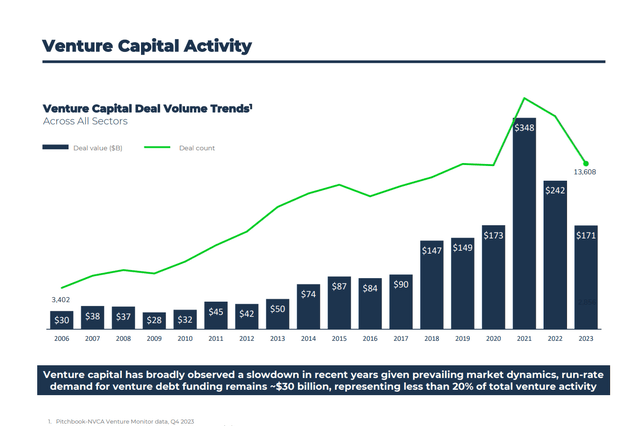

Although 2023 is not a good year for venture capital, bank failure Incidents with Silicon Valley Bank and Signature Bank in March, followed by events at First Republic Bank in May, caused lenders to further hesitate to provide financing to growth-stage companies. This slide from RWAY’s Q4 investor briefing graphically illustrates how venture capital deals will really come to a halt in 2023 after climbing over the past decade.

RWAY Season 4 Demo

As a result, Runway’s focus shifted to credit quality, which resulted in fewer completed transactions in the first half of 2023, particularly as available opportunities did not meet the company’s underwriting standards. During the fourth quarter, the company executed eight transactions involving $154.6 million in financing loans, three of which were new investments.

“In 2023, Runway Growth drove shareholder returns while taking a prudent portfolio management approach as we maintained industry-leading credit quality,” said Greg Greifeld, acting chief executive officer of Runway Growth and deputy chief investment officer and head of credit at Runway. “Growth capital.” …

In 2023, our strategy is to allow for meaningful repayments, reduce our leverage and increase our access to dry powder.

Total investment income in the fourth quarter was $39.2 million and NII was $18.3 million, or $0.45 per share. Net asset value at quarter end was $13.50. Principal repayments received during the quarter totaled $63.4 million.

Fiscal 2023 results include NII of $78.3 million, or $1.93 per share.

Declared a regular dividend of $0.40 per share for the first quarter of 2024, along with a first-quarter supplemental dividend of $0.07 per share.

No loans were placed on non-accrual status as of the quarter-end, however, one loan was placed on non-accrual status after the quarter-end, which may also be part of the reason for the negative market reaction to this loan. Earnings report. Press release:

Effective January 1, 2024, the Company issued a loan to Mingle Healthcare Solutions, Inc. on a non-accrual basis, with an outstanding principal amount of $4.3 million and a fair market value of $3.8 million as of December 31, 2023 Dollar. The loan consists of 0.37% of the total fair value of the Company’s investment portfolio (excluding U.S. Treasury securities) as of December 31, 2023.

In my opinion, this loan is not a huge deal (less than 0.5% of the total portfolio value) and is a typical investment in a venture-stage growth company, but it could be a sign of things to come for other investments in the portfolio question.

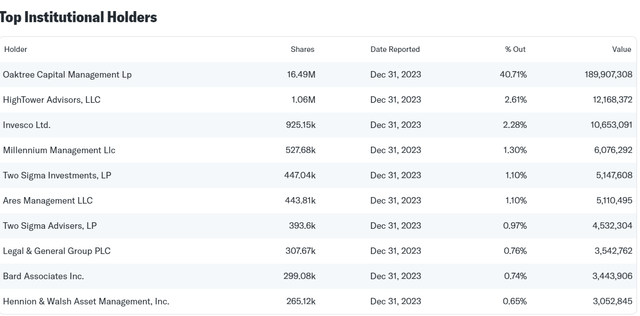

Cash and liquidity at the end of the quarter included $281 million, with an additional $278 million available for borrowings. A secondary offering was completed during the quarter, with Oaktree selling 3.7 million shares of common stock in November. Oaktree has been a partner of Runway since 2016, and despite selling shares in the offering, they still own a significant amount of the stock, accounting for 10% of the shares outstanding as of December 31, 2023, according to Yahoo Finance 40% of the stock.

Yahoo Finance

Acting CEO Greg Greifeld summed up the fourth-quarter results on an optimistic note for 2024:

Our team continues to see substantial opportunity. Despite challenging market and deal activity, our pipeline of qualified, actionable deals has grown relative to 2022. This shows that we have increased discipline and tightened our credit lines. In the first quarter of this year, which tends to be our slowest seasonal quarter, we issued multiple term sheets to new borrowers. Our new joint venture and transaction activity with Cadma has begun rapidly in 2024.

Announcement of new joint venture

On March 7, Runway announced a new joint venture with Cadma Capital Partners. Press release:

“…the Company has entered into a joint venture (“JV”) with Cadma Capital Partners (“Cadma”), a credit venture capital and growth ecosystem affiliate of Apollo Global Management investment platform. Cadma provides asset-backed financing to venture capital and growth lenders, high-growth companies and financial sponsors. “

The new joint venture, Runway-Cadma I LLC, will be an equal partnership between Runway and Cadma. The joint venture has a financing capacity of up to $200 million and will focus on financing privately and sponsor-backed late-stage and growth-stage companies.

According to comments about the new venture in RWAY News, this new revenue stream should result in higher yields than conventional portfolio loans. During the earnings call, Chief Financial Officer Tom Raterman explained how the joint venture would be funded in response to questions:

In terms of how much we put in, initially, we each put in $35 million in equity, and then we arranged financing to probably increase that to $200 million or more. This is the initial cap structure we are considering. In terms of focus, that’s really very much what we’re doing. We see this as an opportunity, especially in a situation where we can’t, won’t enter the stock market, this is an opportunity for us to continue to stay in the market and work with those later-stage companies that tend to have larger deals, through this joint venture, Diversify the portfolio and add new revenue streams through our interest in this joint venture.

Risk and Competition

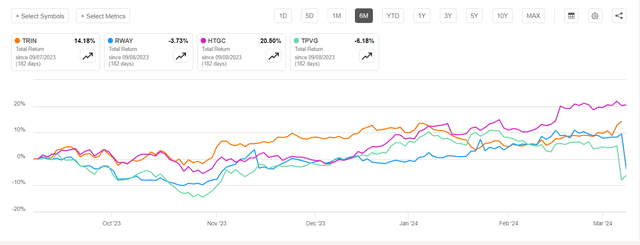

Other BDCs that also provide loans to venture-stage and growth companies such as HTGC, TPVG and TRIN reported mixed results for Q4 and FY23. Although HTGC reported record net profits in Q4 and FY23, net debt investments declined from Q3 to Q4. The overall performance was very good, and the market pushed up HTGC’s stock price after the financial report was released.

TPVG’s March 6 report, on the other hand, was less impressive, with a loss in NAV, a realized loss of $50 million, and an increase in non-cash/PIK income. The price of TPVG also fell after the earnings report was released on March 7.

TRIN reports better than TPVG or RWAY, but probably not as well as HTGC. TRIN’s March 6 report showed NII growth of 15% annually, NAV growth slightly (from $13.17 to $13.19), and total investment commitments reaching a record $340.7 million.

Seeking Alpha

Comparing the total returns over the past 6 months, it is clear that HTGC and TRIN have performed well, while TPVG and RWAY have underperformed.

with Jerome Powell warn congress With more bank failures expected, perhaps the market for venture-stage BDCs will become more cautious overall.In addition, the latest Jobs report calms investor worries A rate cut may be out of the question. But if interest rates do fall in June, it could also have a negative impact on the future profit potential of floating-rate loans held by RWAY.

generalize

Several aspects of the fourth-quarter earnings report, news of a new joint venture committing capital, and concerns about nonperforming loans are all possible reasons for RWAY’s sharp decline today. Coupled with the possibility of rate cuts eroding the company’s future earnings potential, this reaction is somewhat understandable, however, I think the market overreacted and provided income investors with an opportunity to buy shares of well-run BDCs. Chance. Still paying decent dividends.

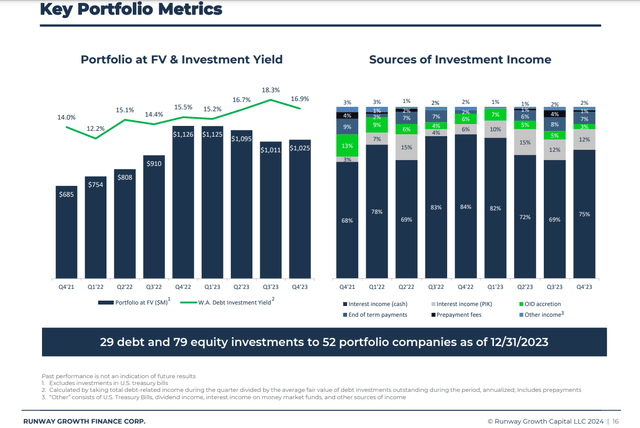

The slideshow below from the Q4 briefing shows the key portfolio metrics investors need to consider before considering a BDC a distressed investment.

RWAY Season 4 Demo

With a fourth-quarter investment yield of 16.9% and strong, diversified investment income streams, RWAY is well-positioned to support continued high-yield dividends, currently based on the latest quarter base dividend of $0.40 (assuming no additional top-up additions) Dividends will be paid at a dividend rate of approximately 14% per year). As a RIC, a company must pay out at least 90% of its taxable income each year. Quarterly NII for the fourth quarter was $0.045 and the underlying dividend was still fully paid. The outlook for 2024 is very positive, with a strong balance sheet, ample available liquidity and the potential for additional high-yield revenue from new joint ventures.

As I wrote this article on Friday, March 8, I considered RWAY’s current market price of approximately $11.50 per share as a Strong Buy. Please do your own research and do not invest without understanding the risks involved.