big river

Last April, I started covering Transocean (NYSE:RIG), which has a “hold” rating on the stock, said that while interest rates have improved during the day, its debt load is an issue. Since then, the stock has fallen more than -20%, while the stock has gained more than 20% S&P. recent, in september, I say its deleveraging story has become clearer, but its valuation and debt make it a high risk/reward stock compared to peers. The stock has fallen -40% since the report. The company recently announced its fourth quarter results, so let’s get to know the company’s name.

Company Profile

As a reminder, RIG owns a fleet of drillships and semi-submersibles outsourced by offshore drilling companies. Drillships are deployed in calm waters, while semi-submersible drillships are deployed in rough sea conditions.

As of the end of 2023, the company has 37 ships with an average age of About 11 years. Its fleet consists of 29 ultra-deepwater vessels and 8 harsh environment vessels. Its 25 ships are in operation, 11 are in cold storage and one is under construction.

Fourth Quarter Results and 2024 Outlook

One of the most important things for RIG remains the daily rate. During 2014, when day rates remained low, the industry and internal IG were under significant pressure due to the pandemic. However, since 2021, interest rates have been rising back up.

In the fourth-quarter report released at the end of February, RIG’s average daily rate increased 24% year-on-year to US$432,000 per day, up from US$349,000 per day a year ago. In the first quarter, its average daily rate was $391,000.

What’s more, RIG said that based on the current backlog, average daily rates are expected to be $433,000 per day in the first quarter of 2024. This would be a 19% increase compared to current levels.

Overall, RIG’s contract revenue increased 22% annually and 4% quarterly to $741 million. Analysts expected revenue of $741.2 million.

Operation and maintenance costs climbed 35% from US$423 million to US$569 million, a quarterly increase of 9%.

Adjusted EBITDA fell -13% to $122 million, a quarterly decrease of -25%.

Adjusted earnings per share loss was -9 cents, compared with -48 cents in the same period last year and -36 cents in the third quarter.

The company generated $98 million in operating cash flow during the quarter. Free cash flow was -$122 million. The company’s full-year operating cash flow was $164 million and free cash flow was -$263 million.

In terms of its balance sheet, RIG ended 2023 with $7.41 billion in debt and $762 million in cash.This equates to leverage of approximately 9x 2023 Adjusted EBITDA of $738 million

RIG noted that contract terms continue to be extended. The company recently contracted a vessel in the Romanian Black Sea for a minimum charter period of 540 days at a daily rate of US$465,000 per day, rising to US$480,000 per day after the initial period.

The company also noted that the U.S. Gulf market, which historically had short delivery times and short contract durations, is now moving toward longer delivery times and longer duration contracts.

Looking ahead, the company expects first-quarter revenue of approximately $780 million. Operating and maintenance expenses are expected to be approximately $545 million and general and administrative expenses are expected to be $47 million.

The company expects full-year revenue of $360 to $3.75 billion. That’s down from an October forecast of 2024 revenue in the range of $3.7-3.9 billion. The company said the reduction in guidance was due to delays in contract start for three vessels due to extended mobilization and contract preparation activities.

In terms of expenses, operating and maintenance expenses are expected to be approximately US$2.2 billion, general administrative expenses are approximately US$196 million, and interest expenses are approximately US$513 million. Capital expenditures are expected to be $242 million.

During the fourth-quarter earnings call, CEO Jeremy Thigpen said:

“With the majority of our fleet under contract through 2024, we continue to aggressively seek work to fill gaps in utilization. That being said, our $9 billion backlog and high-quality assets provide us with capabilities and Flexibility that allows us to selectively pursue the opportunities we pursue while continually striving to strike the right balance between utilization and day rate optimization. As previously stated, we are encouraged by the realization of our long-term plans, The start dates for these programs are far in the future. As we enter 2024 and further into what appears to be an ongoing upgrade cycle, our top priority remains, first, converting our industry-leading backlog into cash. To do this, we will be laser-focused Safety and uptime performance across the fleet, which directly impacts our overall revenue efficiency. Secondly, deleveraging the balance sheet. Assuming the market materializes as we anticipate, we will generate significant free cash over the next several years flow. While we recognize that operating a growing fleet versus deleveraging is a competing priority, we will certainly balance the two in a manner that is most beneficial to our shareholders. Third, ultimately the ultimate goal of managing the business is to serve our shareholders Bring more value, either through share buybacks or dividends.”

RIG continues to benefit from a rebound in day rates, and longer contract terms should start to bring it more visibility. However, operating and maintenance costs have also been soaring, while its operating cash flow has been relatively modest.

With nearly $7 billion in net debt and 9x leverage, the company needs to generate significant cash to pay down debt and begin deleveraging. The company was disappointingly unable to reduce its debt load last year despite a much improved environment and higher day rates as capital expenditure was spent on building new ships.

Lowering revenue guidance while keeping expense guidance unchanged is also not a good thing for a debt-laden company.

Valuation

RIG stock currently trades at nearly 9 times consensus 2024 EBITDA of $1.24 billion and 6.7 times consensus 2025 EBITDA of $1.63 billion.

Its forward price-to-earnings ratio is 12.3 times the consensus 2025 price-to-earnings ratio of 42 cents. Adjusted earnings per share in 2024 are expected to be 1 cent.

Revenue is expected to grow nearly 29% this year and about 12% in 2024.

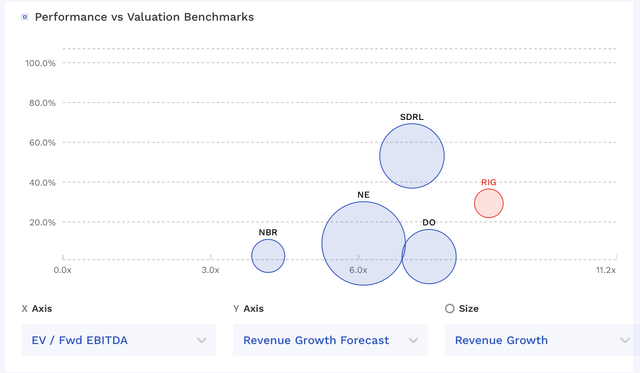

RIG is one of the pricier stocks in the sector, and its debt/equity levels are higher than most of its peers.

RIG valuation compared to peers (fen box)

In order for RIG stock to appreciate, the company really needs to reduce its debt by generating free cash flow. It currently looks like it will be able to generate $450-500 million in free cash flow by 2024. This could see leverage fall to close to 5x by the end of 2024, before strong performance in 2025, with debt likely to be higher in 2025 based on higher EBITDA estimates (helped by firmer daily rates and new rates throughout the year) A reduction of $1 billion. ships) and less capital expenditure. This would reduce leverage to a more reasonable 3.3x. If you maintain 7x 2025 EBITDA estimates, you’re looking at $8 in stock.

in conclusion

In the next two years, the deleveraging path for actual internal growth will still exist. However, the company has indicated that the process may not be smooth. It also needs to continue to see day rates remain strong and keep its operating and maintenance expenses under control.

2024 is a big year for RIG, but so far, it’s not off to a great start. However, if the company is able to start bringing its cold stack rigs back online sometime this year, it could change the company’s image.

RIG remains a high-risk-reward stock. If things go as planned, I think there’s a lot of upside potential, but again, if the market turns, it could be zero given its debt load. I’m leaning more towards the deleveraging story right now, but also recognize the huge risk associated with this name. Therefore, I continue to rate the stock a “Hold.”