Pablo Cuadra/Getty Images Entertainment

Nike stock (NYSE: No) has been hit recently. After years of unstoppable growth, Mr. Market appears to have had a change of heart. But could this pullback create a rare buying opportunity for Legendary?

Let’s break down the numbers and see if Nike is a bargain in disguise. Maybe it’s time to add this stock to your portfolio, or are there better options out there in the athletic apparel industry? Let me know your thoughts in the comments: Do you think Nike is a fading star or a buying opportunity in the making?

real challenge

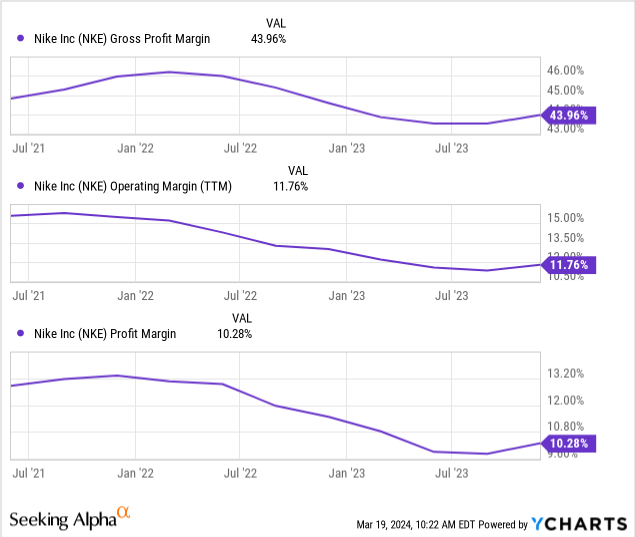

Nike is not immune to the macroeconomic headwinds many companies face. High inflation and ongoing supply chain disruptions have led to rising input costs, squeezing margins in recent years:

chart above While Nike’s bottom line margin decline of 3% was shown to be primarily due to lower gross margins due to higher input prices and lingering supply chain issues, readers should note that Nike’s operating efficiency also appears to have deteriorated somewhat. The company’s trailing-twelve-month operating margin fell 4% since 2021, as evidenced by this.

Global supply chain difficulties remain a major challenge for Nike. While the worst damage from the pandemic may have eased, geopolitical tensions and unpredictable transportation costs continue to create uncertainty. These factors make it more expensive for Nike to produce footwear and apparel, ultimately forcing the company to either absorb those costs or risk alienating consumers with higher prices, which will come into play in the next section.

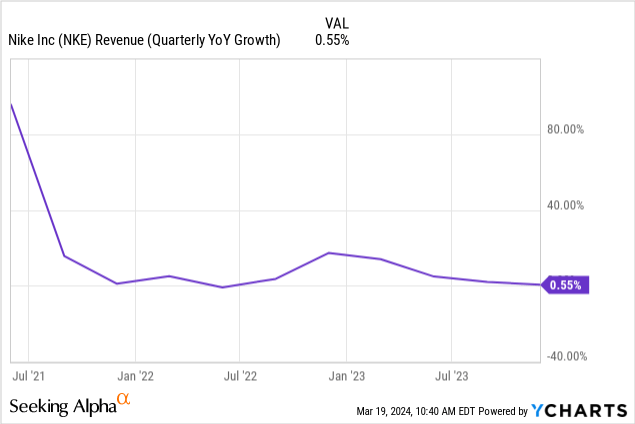

Revenue growth is slow

The company experienced significant revenue growth early in the pandemic, driven by demand for athleisure and at-home workout apparel; however, economic uncertainty, supply chain disruptions, and inflationary pressures have weighed on growth in recent years:

Nike faces continued headwinds in 2024 due to lingering supply chain issues and slowing consumer spending, but analysts expect a better 2025 as China reopens, Nike direct-to-consumer boosted by investors and potentially alleviated inflationary pressures.

Yahoo Finance

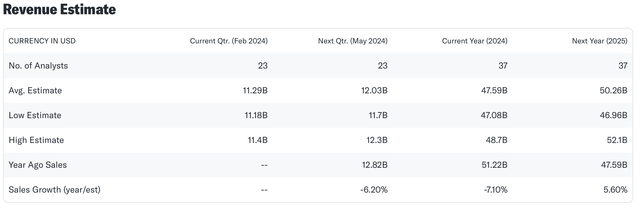

Although Nike is year-round guide Despite the downward revision, there is still potential for growth in specific geographies and sales pipelines in 2025, as the company’s management discussed in detail during its last earnings call.

management action

In order to drive revenue growth, Nike has placed a strong emphasis on direct-to-consumer sales channels, allowing them to capture a greater proportion of profits, and recent results are encouraging: Nike direct revenue was $5.7 billion, up 6% as reported, in It rose 4% on a currency-neutral basis.

Nike’s push into direct-to-consumer sales has been largely successful, as direct sales have grown faster than overall revenue, suggesting the shift is paying off. The company continues to invest in creating digital and physical shopping experiences for consumers under this model.

Additionally, as management discussed in its most recent earnings report, the company is focusing resources on key growth categories such as women’s activewear, Jordan Brand and fashion-forward activewear call:

First, let’s talk about the women’s business, which is already about a $9 billion business, and that’s just the NIKE brand, excluding Jordan and Converse. Our women’s business has averaged high single-digit growth over the past three years. While we’re encouraged by this progress, we’ve now seen what we believe is the best plan to accelerate the growth of women’s businesses. Our program gives us more confidence to serve her through sports and fashion. Today, approximately 40% of our members are female consumers. They make up a larger proportion of new members, and member demand grows faster.

On the cost front, management is targeting cumulative cost savings of up to $2 billion over the next three years and lists the following target areas: simplifying product assortments, improving supply chain efficiency, leveraging scale to reduce operating marginal costs, and increasing automation Data and technology bring speed, streamline organizational structures, reduce management layers, and improve procurement capabilities.

While I acknowledge the potential benefits of Nike’s direct-to-consumer strategy and cost optimization measures, I remain cautious about its near-term impact on revenue growth. It remains to be seen whether the gains from direct sales can fully offset potential losses in the wholesale market.

Additionally, I’m interested in observing the long-term impact of cost-cutting measures. I want to ensure that these efforts contribute to sustainable profitability and do not compromise workforce stability or product quality.

For now, I recommend taking a wait-and-see approach and re-evaluating Nike’s performance in the coming quarters to get a clearer picture of the success of these strategies.

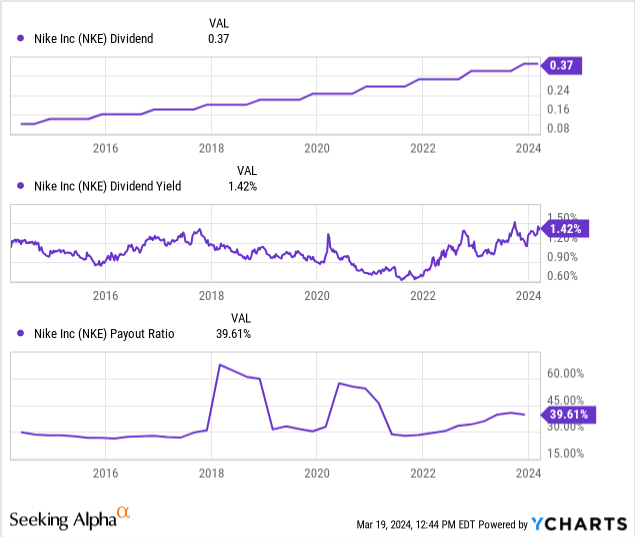

Dividend Yield and Safety

Over the past decade, Nike’s quarterly dividend has grown steadily:

Although Seeking Alpha Quant gives Nike an unfavorable “D” rating for its dividend safety, I believe the dividend is safe for now. While the payout ratio does fluctuate, and Nike’s yield is lower than other companies in the consumer discretionary industry, there are several reasons to be cautiously optimistic.

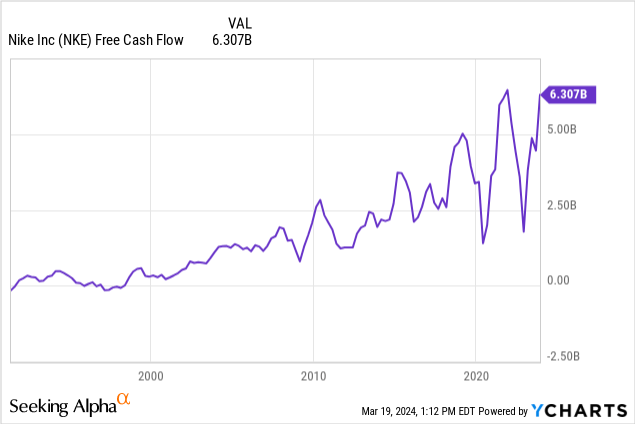

Nike has a long history of increasing its dividend, demonstrating its commitment to returning value to shareholders. Additionally, Nike maintains a healthy balance sheet and generates positive cash flow, providing financial flexibility.

Nike’s current dividend appears to be safe for the foreseeable future, but the economic headwinds I discussed in my recent article, “The Job Market Is Softening,” could affect the company’s dividend growth trajectory.

Valuation

Nike’s valuation presents a mixed picture. The stock currently trades at about 29 times earnings, slightly below its historical average. This could signal an opportunity if earnings growth rebounds in the future; however, continued economic uncertainty and rising input costs cloud the outlook.

Given these factors, along with Nike’s strong brand, growth potential in emerging markets, and focus on direct-to-consumer sales, I believe a reasonable near-term price target is between $70 and $80, reflecting a more reasonable 20x P/E ratio Given the significant execution risks and macroeconomic headwinds the company faces.

in conclusion

Nike is undoubtedly an iconic company with lasting brand power. However, economic headwinds and lingering supply chain issues pose real challenges to its current growth trajectory. While the direct-to-consumer push and expansion into promising markets offer potential, the success of these strategies may take time to fully materialize. Additionally, the execution of cost-saving programs needs to be carefully considered to avoid negative impacts on product quality or labor.

Investors must weigh a company’s potential against the risks involved. At its current valuation, Nike stock is not cheap. However, if the company successfully navigates the volatile economic environment and demonstrates renewed earnings growth, a price target in the $70 to $80 range could provide an attractive entry point.