Photography by Denis Dieter

While shares of GameStop Corp. are nowhere near the peaks reached during the 2021 meme stock craze, GameStop Corp.NYSE: GMEI think when it releases Q4 and 2023 full year results March 26 After market close. Analysts expect the video game retailer to report fourth-quarter revenue of $2.05 billion and earnings of $0.25 a share, while full-year estimates are for revenue of $5.53 billion and earnings of $0.13 a share.

That said, I expect GameStop to beat analysts’ expectations due to stronger video game sales during the holiday season compared to 2022. While my model predicts another year-over-year decline in sales, I don’t think the expected decline is deep enough to warrant the stock trading at a discount relative to its peers.Therefore, I rate GameStop a Buy with a price target of $21.18 per share, up 62% from current levels.

Video game sales rebound

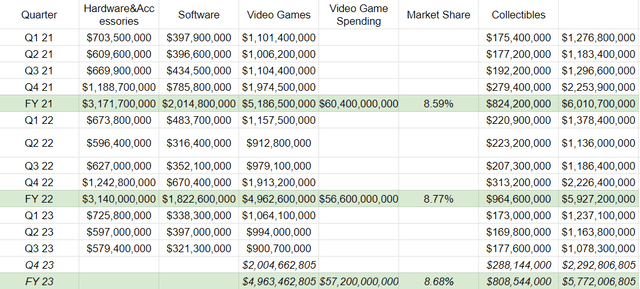

Because GameStop is a video game retailer, the company’s sales are affected by the strength of consumer spending on video games. In 2021, U.S. consumers will spend on video games $60.4 billion It was driven by strong demand for next-generation gaming consoles PlayStation 5 and Xbox Series X.

However, U.S. consumer spending on video games will drop 5% in 2022 compared with the same period last year $56.6 billion Mainly due to a series of new product launches and macroeconomic conditions causing consumers to change their consumption patterns. As a result, GameStop’s 2022 sales fell 1.4%. While some may argue that GameStop’s sales decline is primarily due to its outdated brick-and-mortar business model, I disagree as the need to purchase video games from brick-and-mortar stores still exists.

A poll A YouGov survey last August found that 16% of American gamers prefer to buy video games in physical stores.Given that the number of video game players in the United States is estimated to be 212.6 millionwhich means GameStop has a potential market of more than 34 million gamers in the United States.

With this in mind, U.S. video game spending grew to $57.2 billion in 2023, driven by a strong holiday season, with video game sales reaching $7.91 billion between November 26 and December 30.Video game sales surge in 2023, according to Mat Piscatella, executive director of Circana Video Games because “One of the best releases in the history of the industry.”

revenue forecast

The above information is critical to forecasting GameStop’s fourth quarter and full-year 2023 revenue. GameStop generates revenue by selling hardware, accessories, software and collectibles. The video game segment of the company’s revenue includes hardware, accessories and software. Meanwhile, the collectibles segment includes sales of action figures, replicas and trading cards.

As far as the video game sector is concerned, GameStop’s revenue from hardware, accessories and software accounted for 8.59% of total video game spending in 2021 and 8.77% in 2022. Therefore, I forecast GameStop’s share of total video game spending in 2023 to be 8.68%, the average share over the past two years. Based on this, I expect GameStop’s full-year revenue from hardware, accessories, and software to reach $4.9 billion, which will result in the segment’s revenue of just over $2 billion in the fourth quarter of 2023.

GME Profit Report

As for the collectibles sector, toy sales reject Growth of 8% in volume and dollar terms by 2023. Even during the holiday season, toy sales were down 8% in dollar terms and 6% in volume terms. This means shoppers are buying fewer toys at lower prices, buying cheaper toys. Therefore, given GameStop’s collectibles revenue, I predict that its collectibles revenue will decline by 8% annually 28% market share The collectible toy market in the United States. Such a decline would mean my forecast for GameStop’s full-year 2023 collectibles revenue is $808.5 million, with fourth-quarter revenue of $288.1 million.

Based on my predictions for GameStop’s video game and collectibles segment, I expect the company’s fourth-quarter revenue to be close to $2.3 billion and full-year revenue to reach $5.7 billion. Those figures were higher than analysts’ expectations of $2.05 billion and $5.53 billion, respectively.

|

income part |

Season 4 |

annual |

|

video games |

$2,004,662,805 USD |

$4,963,462,805 |

|

Collection |

$288,144,000 USD |

$808,544,000 |

|

Total revenue |

$2,292,806,805 USD |

$5,772,006,805 USD |

EPS forecast

Looking at the rest of GameStop’s income statement, the company’s average gross margin for the first three quarters of 2023 was 25.1%, which is my fourth-quarter gross margin forecast. This is in line with GameStop’s historical performance, as the fourth quarter’s gross profit margin was lower than the third quarter, and the full year gross profit was 25.18%. Therefore, I expect the company’s cost of revenue to be $1.7 billion and $4.3 billion for the fourth quarter and full year, respectively, and gross profit to be $362.8 million and $1.3 billion, respectively.

|

quarter |

income |

cobalt |

gross profit |

Gross profit margin |

|

Season 1 21 |

US$1,276,800,000 |

$946,700,000 |

$330,100,000 |

25.85% |

|

Season 2 21 |

US$1,183,400,000 |

US$862,500,000 |

$320,900,000 |

27.12% |

|

Season 3 21 |

US$1,296,600,000 |

$978,000,000 |

US$318,600,000 |

24.57% |

|

Season 4 21 |

US$2,253,900,000 |

US$1,875,700,000 |

US$378,200,000 |

16.78% |

|

FY21 |

US$6,010,700,000 |

US$4,662,900,000 |

$1,347,800,000 |

22.42% |

|

Season 1 22 |

US$1,378,400,000 |

$1,079,900,000 |

US$298,500,000 |

21.66% |

|

Season 2 22 |

$1,136,000,000 |

US$853,800,000 |

US$282,200,000 |

24.84% |

|

Season 3 22 |

US$1,186,400,000 |

US$894,800,000 |

$291,600,000 |

24.58% |

|

Season 4 22 |

US$2,226,400,000 |

US$1,726,600,000 |

$499,800,000 |

22.45% |

|

FY22 |

US$5,927,200,000 |

US$4,555,100,000 |

US$1,372,100,000 |

23.15% |

|

Season 1 23 |

US$1,237,100,000 |

$949,800,000 |

US$287,300,000 |

23.22% |

|

Season 2 23 |

US$1,163,800,000 |

US$857,900,000 |

US$305,900,000 |

26.28% |

|

Season 3 23 |

US$1,078,300,000 |

US$796,500,000 |

US$281,800,000 |

26.13% |

|

Season 4 23 |

$2,292,806,805 USD |

$1,714,698,633 USD |

$578,108,172 USD |

25.21% |

|

FY23 |

$5,772,006,805 USD |

$4,318,898,633 |

$1,453,108,172 USD |

25.18% |

For operating costs, the company only recognizes cost of sales, general and administrative costs and asset impairment. Since the company hasn’t recognized any impairment charges since Q4 2022, I don’t expect any impairment charges in 2023.

As for selling, general and administrative costs, GameStop will control this cost to 27% of revenue in the first three quarters of 2023. At the same time, due to the seasonality of GameStop’s business, the cost increased by 22.37% sequentially in the fourth quarter. Based on this, I estimate selling, general and administrative costs for the fourth quarter to be $362.8 million and for the full year to be $1.3 billion.

|

quarter |

Selling and administrative expenses |

Month-on-month change |

|

Season 1 21 |

$370,300,000 |

|

|

Season 2 21 |

$378,900,000 |

2.32% |

|

Season 3 21 |

$421,500,000 |

11.24% |

|

Season 4 21 |

US$538,900,000 |

27.85% |

|

FY21 |

US$1,709,600,000 |

– |

|

Season 1 22 |

$452,200,000 |

-16.09% |

|

Season 2 22 |

US$387,500,000 |

-14.31% |

|

Season 3 22 |

US$387,900,000 |

0.10% |

|

Season 4 22 |

$453,400,000 |

16.89% |

|

FY22 |

US$1,681,000,000 |

– |

|

Season 1 23 |

$345,700,000 |

-23.75% |

|

Season 2 23 |

$322,500,000 |

-6.71% |

|

Season 3 23 |

US$296,500,000 |

-8.06% |

|

Season 4 23 |

$362,825,125 |

22.37% |

|

FY23 |

$1,327,525,125 USD |

– |

Based on my forecasts, I expect GameStop to report operating income of $215.2 million in the fourth quarter and $125.5 million for the full year, with operating margins of 9.4% and 2.2%, respectively.

|

quarter |

gross profit |

% of revenue |

derogation |

Operating income/loss |

Operating profit margin |

|

Season 1 21 |

$330,100,000 |

29.00% |

$600,000 |

-$40,800,000 |

-3.20% |

|

Season 2 21 |

$320,900,000 |

32.02% |

$0 |

-$58,000,000 |

-4.90% |

|

Season 3 21 |

US$318,600,000 |

32.51% |

$0 |

-$102,900,000 |

-7.94% |

|

Season 4 21 |

US$378,200,000 |

23.91% |

$6,100,000 |

-USD 166,800,000 |

-7.40% |

|

FY21 |

$1,347,800,000 |

28.44% |

$6,700,000 |

-$368,500,000 |

-6.13% |

|

Season 1 22 |

US$298,500,000 |

32.81% |

$0 |

-USD 153,700,000 |

-11.15% |

|

Season 2 22 |

US$282,200,000 |

34.11% |

USD 2,500,000 |

-$107,800,000 |

-9.49% |

|

Season 3 22 |

$291,600,000 |

32.70% |

$0 |

-$96,300,000 |

-8.12% |

|

Season 4 22 |

$499,800,000 |

20.36% |

$200,000 |

$46,200,000 |

2.08% |

|

FY22 |

US$1,372,100,000 |

28.36% |

$2,700,000 |

-$311,600,000 |

-5.26% |

|

Season 1 23 |

US$287,300,000 |

27.94% |

$0 |

-$58,400,000 |

-4.72% |

|

Season 2 23 |

US$305,900,000 |

27.71% |

$0 |

-$16,600,000 |

-1.43% |

|

Season 3 23 |

US$281,800,000 |

27.50% |

$0 |

-$14,700,000 |

-1.36% |

|

Season 4 23 |

$578,108,172 USD |

15.82% |

$0 |

$215,283,047 USD |

9.39% |

|

FY23 |

$1,453,108,172 USD |

23.00% |

$0 |

$125,583,047 USD |

2.18% |

This leaves interest income, other losses and tax benefits to be projected on GameStop’s income statement. For these items, I will use the same numbers as Q3 2023. However, these items may differ from my forecasts depending on how GameStop manages its cash holdings in the fourth quarter of 2023.

Therefore, I expect GameStop’s fourth-quarter net profit to be $226.8 million, full-year net profit to be $170.4 million, and earnings per share to be $0.74 and $0.56, respectively. Those forecasts were higher than analysts’ expectations for fourth-quarter earnings of $0.25 per share and full-year earnings of $0.13 per share.

|

Q4 2023 |

fiscal year 2023 |

|

|

income |

$2,292,806,805 USD |

$5,772,006,805 USD |

|

cobalt |

$1,714,698,633 USD |

$4,318,898,633 |

|

gross profit |

$578,108,172 USD |

$1,453,108,172 USD |

|

Selling and administrative expenses |

$362,825,125 |

$1,327,525,125 USD |

|

operating income |

$215,283,047 USD |

$125,583,047 USD |

|

interest income |

$12,900,000 |

$47,100,000 |

|

Other losses |

USD 2,500,000 |

$4,900,000 |

|

Pre-tax income |

$225,683,047 USD |

$167,783,047 USD |

|

Tax incentives |

$1,200,000 |

$2,700,000 |

|

net income |

$226,883,047 USD |

$170,483,047 USD |

|

operating system |

305,514,315 |

305,514,315 |

|

Earnings per share |

$0.74 |

$0.56 |

Valuation

According to my forecast, GameStop’s EV/sales multiple will be 0.62, compared to the industry average of 1.29. That said, I believe the company should still trade at a discount relative to its peers due to lower sales, which is why I target an EV/sales multiple of 1. Therefore, my price target for GameStop is $21.18 per share, implying a 62% upside from the current stock price of $13.10.

|

Estimated sales |

$5,772,006,805 USD |

|

electric car |

US$3,570,000,000 |

|

Electric Vehicles/Sales |

0.62 |

|

industry average |

1.29 |

|

Multiple goals |

1 |

|

price target |

$21.18 |

|

Upside |

62% |

risk

Since the core of my bullish case for GameStop is its potential to beat analysts’ estimates when it reports full-year financial results, risks to my thesis include an expected slowdown in video game spending this year due to weaker launch plans than in 2023. Circana’s Mat Piscatella predicts video game spending will reach 2024 decline Growth of 2% to 10% compared with the same period last year. However, Piscatella expects spending to rebound in 2025 due to the highly anticipated release of GTA VI.

Another risk facing GameStop is a new investment policy that allows CEO Ryan Cohen and the management team to invest in the same securities as the company, rather than the previous policy of investing in investment-grade short-term income securities. So if GameStop’s investments go awry, its cash balance of $909 million could dwindle quickly.

in conclusion

With the stock trading near multi-year lows, I believe GameStop could be an opportunity at current levels ahead of its March 26 earnings report. As it stands, I expect the company’s revenue and EPS to beat analysts’ expectations for holiday season game sales given the strong video sales, in addition to its prudent cost management. Given that GameStop’s stock price has fallen significantly relative to its peers, I rate it a Buy with a price target of $21.18 per share, which implies 62% upside potential from its current valuation.