Userba011d64_201/iStock via Getty Images

Style regimes are one of the biggest risk factors for investors, second only to overall stock risk. After 15 years of dominance by growth styles, the return of intra-market volatility has sparked renewed interest in style frameworks and cyclical rotations.By re-recognizing oneself Through the dynamics of style cycles, we can better understand how these portfolio construction models shape our financial future.

In this analysis, I will demonstrate that style returns are the market’s veritable Gulfstream and that investors should not ignore its powerful current. I will address three basic but fundamental questions:

1. What is the typical duration of a Growth and Value Style System?

2. How significant is the swing between growth and value?

3. What is the mechanism of style change?

With its three simple yet powerful inputs, I believe the Russell-style approach can reveal something about the market The behavior that resonates most.

What is the typical duration of a Growth and Value Style System?

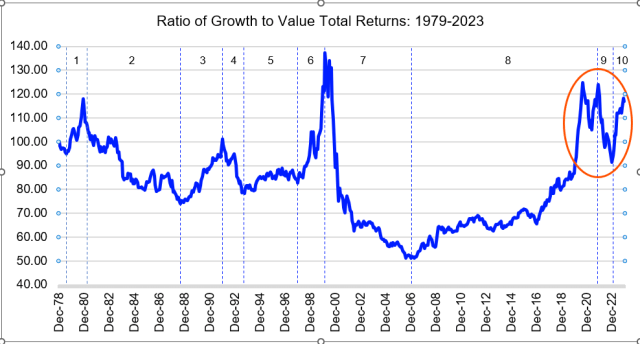

The sharp rotation into value stocks in 2022 is also fresh in the mind, and investors are wondering whether this rotation is a temporary move or a lasting market trend.To provide context and guidance, I measured total return Russell 1000 Growth and Value Index From December 1978, it was rescaled to 100 as the initial value.

This approach allows us to look at different periods of growth or value outperformance without distracting from the runaway compounding of stock returns. The method is time-independent: comparisons across periods, such as between the 1980s and the 2010s, can be made on a roughly equivalent basis.

Description of the Russell 1000 Growth Index total return divided by the Russell 1000 Value Index total return, with parity set at 100 and a start date of December 31, 1978. (Source: FTSE Russell data, February 2024.)

By connecting the peaks and troughs in the chart above, 10 discrete periods of style performance can be easily identified. An uptrend indicates growth outperformance, while a downtrend signals a shift toward value. Fascinatingly, this clear cyclical pattern emerges despite the fact that month-to-month style returns consistently move in the same direction only 51.9% of the time – a rate not unlike flipping a coin!

Some model judgment is necessary when specifying a style system. For example, in the 1990s, stages five and six were separated rather than calculated as a combined growth stage because these two stages were more distinct than average growth and value. Notwithstanding this discretion, the framework provides an evidence-based approach to decomposing the volatility function of style returns.

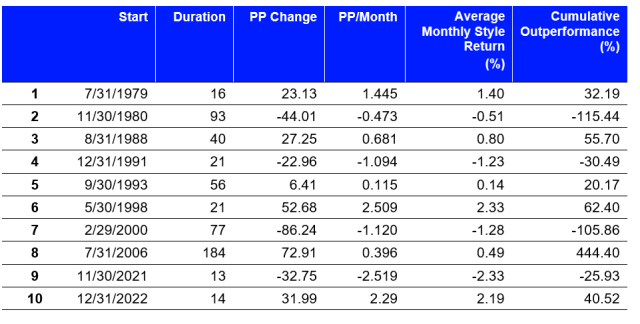

Four different measures of trend size and strength are described. PP Change represents the percentage change in the total return of the Russell 1000 Growth & Value Index during each regime period. The PP/month column is the rate of change from the previous value and is also the average slope for each state. System 10 is still in the interim stage and does not mean that the system is complete. (Source: FTSE Russell, February 2024.)

The average duration of style status is 64 months, but there’s more nuance than that headline number suggests. First, the length of the system varies greatly, from 13 months at the short end (system nine) to 184 months at the long end (system eight). The difference is more than an order of magnitude.

In fact, the 15-year Great Growth Regime (GGR, Regime Eight), which lasted from July 2006 to November 2021, was a real outlier that skewed the overall results. Notably, state eight is 2.3 standard deviations away from the mean state length (4.6 if excluded from the sample).

By isolating the effects of GGR for 15 years, we gain a more representative understanding of style system length. The overall average cycle length shortened to 46 months, and the average duration of the growth cycle almost halved to 33 months. Therefore, we can conclude that style systems are not a phenomenon of the month, but are usually multi-year trends. Furthermore, when GGR is excluded, value systems tend to last twice as long as their growth brethren.

How significant is the swing between growth and value?

After 44 years, the annualized returns of these opposing strategies differ by just 42 basis points, and growth and value recently achieved return parity on March 14, 2023. If two stylistic approaches take investors to roughly the same destination, how important is style to trend? Are they just ripples on the surface of stock returns overall?

A more appropriate term would be “powerful waves”: oscillations between growth and value that can have huge consequences. Calculating the growth rate versus the rate of change in total value returns shows that style trends progress at an average rate of 1.15 percentage points per month (pp/m).

For context, this style trended 44% faster than the stock market’s expected monthly returns, while its volatility was only 55% of the latter. This analysis shows that style trends are stronger and more consistent than trends in the underlying stock market. Taken together, these fluctuations equate to a monthly redistribution of $600 billion in shareholder wealth between growth and value.

Although the growth/value total return rate of the average style system fluctuates by 40.9 percentage points, the pace of style returns at the style system level varies greatly. Historically, value systems have progressed 26% faster than growth systems due to the rapid return of value after growth trends peak.

Excluding the stylistically neutral fifth style of the mid-1990s (which had a progression rate of only 0.12 pp/m), GGR is the least dynamic style trend, with a progression rate of only 0.39 pp/m. Compare this slow pace to the next value cycle (9th in the table), which was the most aggressive ever, surging at negative 2.52pp/m. This reversal in style direction after a 15-year period of stability, as well as the six-fold strengthening of the style, has caused many stock investors to experience a sense of market violence in 2022.

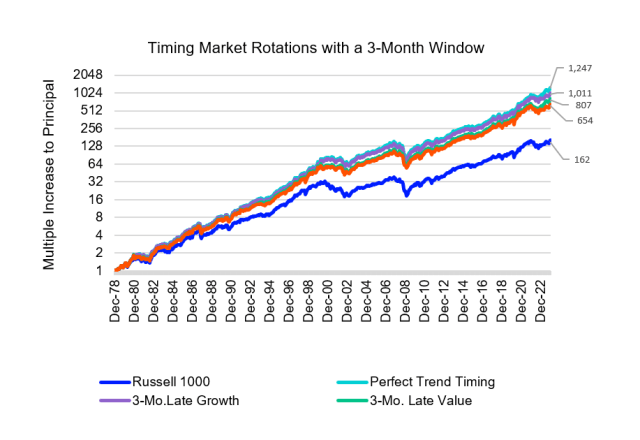

Perfectly timing these 10 Russell-style systems has meant that underlying index returns have increased nearly sevenfold since 1979, with investor gains soaring from 162 times initial capital to a staggering 1,247 times. Even if investors missed these shifts due to the 3-month delay, they would still have experienced a fourfold increase in Russell 1000 Index returns, a 653x appreciation. By comparison, an extremely unlucky investor who is consistently out of step with prevailing style trends would only earn 10.5% of the benchmark return. In short, style allocation matters – but how do investors profit from these key moments of style shifts?

What is the mechanism of style change?

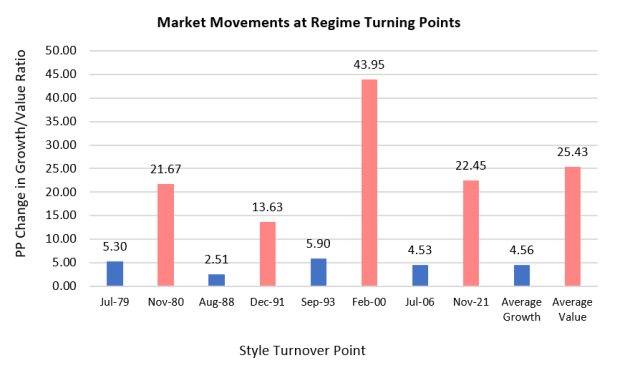

The main difference between transitions from growth to value and from value to growth is their dynamism. Value shifts are consistently more dramatic events, averaging 5.57 times larger than market style shifts. This value is calculated by measuring the total change in growth ratio and total value return in the three months before and after each style’s maximum or minimum. Essentially, it captures the breadth of market coverage during the transition period from a style perspective.

The clear conclusion is that, unlike decaying U-shaped growth transitions, value rotations are quite dramatic market events. While investors have had time and opportunity to assess risk and reposition when growth returns favorably, they do not have such a luxury of value returning.

The total market movement (in absolute value) 3 months before and after each style system transition point, extreme value, expressed as the percentage change in the ratio of Russell 1000 Growth to Russell 1000 Value Index total returns. Blue indicates growth conditions and rising value conditions (Source: FTSE Russell, February 2023.)

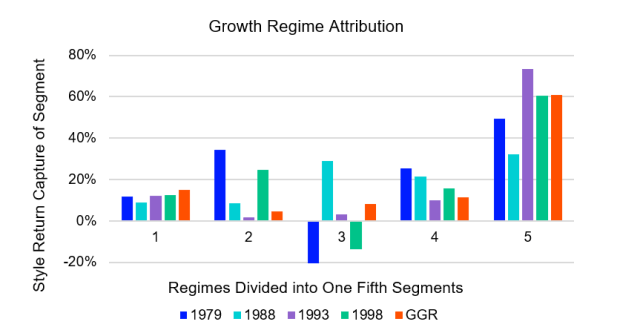

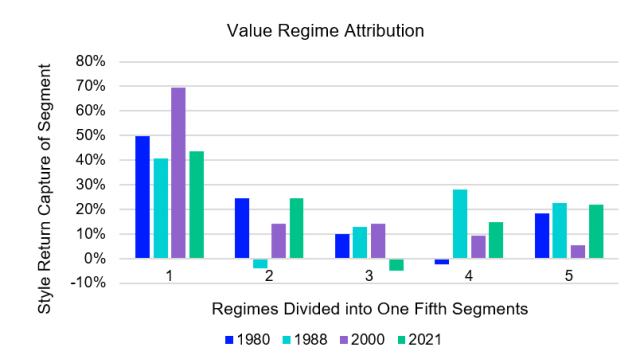

Why is the intensity of rotation so different? It stems from a basic characteristic of all growth models – as style trends peak, returns soar. No growth cycle ends without this final boom. In fact, the last 20% of growth trends account for 50.8% of style returns. The risk enthusiasts among us can rejoice because during these growth spurts, style returns accrued 6.23 times faster than the returns recorded during the rest of the regime.

Growth and value systems are divided into fifth buckets over time, illustrating their capture rate of overall system style returns. Source: FTSE Russell, February 2024.

Perhaps as striking as the regularity and predictability of these growth bursts is the symmetry of the ensuing collapse in growth and recovery in value. Just as the growth mechanism’s style returns are backloaded through the cycle, the value mechanism’s return is similarly 50.8%.

This terminal growth peak not only creates a pattern that reverberates throughout the history of style cycles, but also shows how far ahead the market rotation is in predicting the strength of the move into the next cycle.

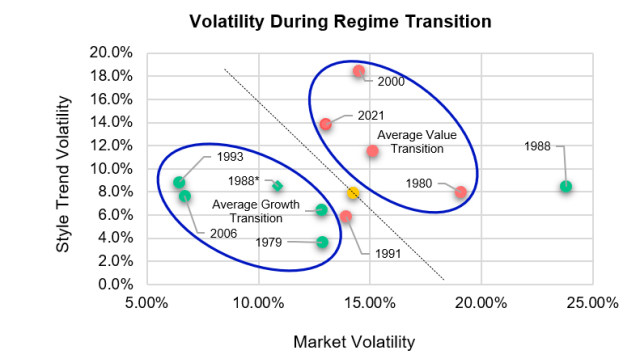

Additionally, we can use a volatility perspective to corroborate this U- versus V-shaped growth framework and value style shifts. An evaluation of the six months that included each style rotation found that market volatility and style volatility were 1.4 percentage points below average during the shift to growth, while these volatility measures increased by 0.9 and 3.6 points, respectively, during the shift to value. percentage points.

To add context, these numbers show that the growth transition for style trend volatility dropped to the 48th percentile, while the value transition hit the 86th percentile. In other words, the transition from value to growth and the transition from growth to value are two completely different animals.

The green dot represents the growth mechanism and the red dot represents the value cycle. Data observations are based on the average volatility over the 7 months encompassing each transition point (3 months before, transition month and 3 months after). (Source: FTSE Russell data, February 2024.)

Style works in your favor

Style cycles are long-lasting, multi-year trends that represent powerful undercurrents beneath the surface returns of the stock market. Given the importance of style returns and their associated volatility patterns, the most risk-efficient way to benefit from style shifts is to actively allocate value following corresponding regime changes.

Not only do these style shifts provide clear market signals when they occur, but value style returns experience early cycle concentration and diminish in intensity as the shift progresses. Additionally, the eventual return to growth has historically been a gradual process, reducing the risk for investors of over- or under-performing a style shift.

To further my understanding of the growth and style approach and its practical application, I wrote Three papers in a series of fouravailable from FTSE Russell’s Research Library.

Editor’s note: Summary highlights for this article were selected by Seeking Alpha editors.