Diane 39

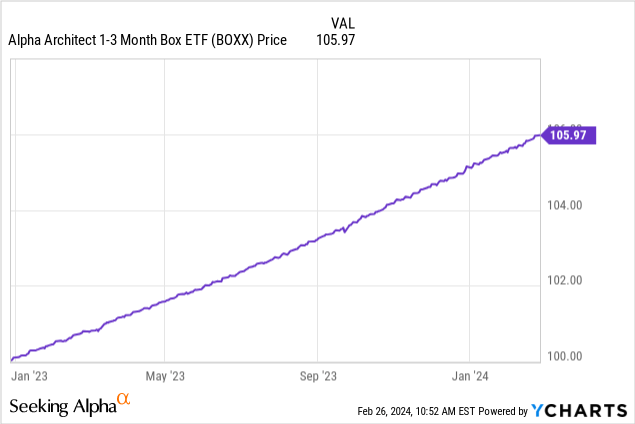

Sometimes you ponder a question for years and then find the answer when you least expect it. While reading Bloomberg on a leisurely weekday afternoon last week, I discovered an interesting fund that solved a puzzle I’d been researching for a long time. long time. The fund is Alpha Architect 1-3 Month Box ETF (Bat: BOXX).Last week, Bloomberg Fund Introduction and its manager Wesley Gray, a former U.S. Marine Corps intelligence officer turned finance professor. The idea behind the ETF is simple – it uses a simple options strategy called a box spread to earn a cash return, but tax-deferred. While it may not sound significant, the fund makes a difference in an investor’s ability to maintain after-tax wealth ahead of inflation.

Problem: The government candle burns at both ends

if you have If you have significant wealth and live in a high-tax jurisdiction, maintaining your standard of living over time is no easy task. For example, in California, the marginal income tax rate on ordinary income for wealthy investors is 37%, the federal income tax and Medicare surtax are 3.8%, and the state income tax is 13.3%. Overall, these increases result in a marginal income tax rate of 54.1%.

While we shouldn’t shed a tear over movie stars and rappers paying these income tax rates, they create a huge problem for investors because the returns ignore the effects of constant redistribution of wealth through money printing/inflation. Inflation has calmed down a bit recently, but over the past 12 months, the US inflation rate was 3.1%. So if your after-tax profit last year was 3.1%, you’ve only maintained your purchasing power. This means that if all of your earnings were taxed at the top ordinary income rate, you’d need to earn about 6.75% or you’d go backwards. Add to that a family’s property taxes and health insurance premiums of over $20,000 per year (the government doesn’t call it a tax, but it is), and it’s not difficult to create a situation where a family has a lot of assets and a low tax rate. The return on investment is close to or higher than 100%. This is where the rich have to start playing defense. Dividends and long-term capital gains are taxed at a lower rate, and capital gains are deferred until sale. Municipal bonds can also provide tax shelter.

These types of strategies also come in and out of fashion. In the 2010s, stock valuations were quite reasonable, but municipal bond yields were low—0-1% after inflation. Today, stock valuations are approaching dot-com bubble levels, but you don’t have to be a part of it if you don’t want to, as bond yields on bonds and cash have risen significantly. Today, you can earn a compound return of nearly 5.5% with a Vanguard money market fund, but whether that’s good for you after-tax depends on your tax rate. This is a problem that doesn’t have a good solution so far.

Think outside the box

So how does BOXX solve some of these problems for us? Matt Levine is a popular columnist who worked as a lawyer and derivatives salesman for Goldman Sachs.Levine Provides lengthy explanation In his own review of BOXX he explains how BOXX works.

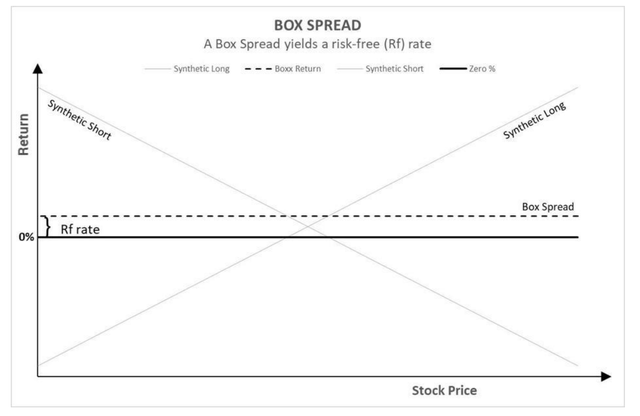

I’ll provide my own explanation. Since options provide leverage, cash returns are priced in the options market – otherwise, you could trade free money arbitrage for large trades. A call option “pays” the cash rate, while a put option “earns” the cash rate. Additionally, long calls make money when the stock goes up, and long puts make money when the stock goes down. By buying and selling offsetting options, price risk can be completely offset, leaving only the time value of money.that’s the point box spread– It offsets the price risk of the underlying to obtain a risk-free rate.

Box Spread Profit Chart (BOXX Prospectus)

The fund performs box spread trades on the S&P 500 Index (SPY) and, to a lesser extent, Booking Holdings (BKNG). Booking Holdings was chosen for its high share price and liquidity in a small subset of its trades, which help the fund pay taxes.

The current annual yield rate of the BOXX basic transaction is 5.67%, minus the annual fee of 0.19%, and the net effective expected return rate is 5.48%.

So how is this better than money market funds? By using box spreads, we have just converted interest income into capital gains. Of all investment income, interest income is the worst taxed, while long-term capital gains are the best taxed. BOXX goes a step further and uses its unique ETF structure to avoid distributing any capital gains to investors. This creates many interesting possibilities.

- If you have capital gains tax loss carryforwards, they do not exempt you from paying interest taxes in future years. However, with box spreads, you will receive tax-free income until your tax loss carryforward is exhausted. This made box spreads popular again with ultra-high-net-worth investors after the 1987 stock market crash and dot-com bubble burst.

- You can realize long-term capital gains on BOXX by holding it for at least one year. You can also push income into future years by not realizing gains until your tax bracket drops.

- Rather than being taxed on a cash basis like when interest is earned, a box spread allows you to sell only a small portion to cover living expenses, while the rest compounding is tax-free. This mirrors the stock market and avoids the negative tax treatment of interest.

- Long-term capital gains and dividends are taxed at 0%, which will be phased out if you make too much ordinary income. If you plan carefully, you may be able to pay 0% capital gains tax on up to $47,000 of taxable income for an individual, or up to $94,000 of taxable income for a married couple filing jointly. Box spreads give you more control over your taxable income, so you can sometimes cash out here. It’s not something I would stress about, but sometimes it creates opportunities to make or save $5,000-10,000.

BOXX Practice

Let’s say you sell a business for $10 million after taxes and live in California. You’re going to see a lot of crypto kids driving around in Lamborghinis again and they’re worried about the stock market going into a bubble. If you put all your money into stocks, history shows that poorly timed purchases can land you in a bear market, causing you to lose 50% of your investment. If you put your money into bonds or cash, you’ll pay a very high marginal income tax.

Let’s do some integers to illustrate.

- You invest $10,000,000 in a money market fund at the beginning of the year.

- This will give you $550,000 in interest income.

- You pay a 40% federal/state tax rate on $220,000.

- Your after-tax income is $330,000.

- Inflation is 3% or $300,000, so your net gain in after-tax purchasing power is $30,000. Taking inflation into account, your “total effective tax rate” is 95%.

Now let’s redo this example using a box spread.

- You invest $10,000,000 in BOXX

- By the end of the year, BOXX has appreciated to $10,550,000.

- You have insurance this year, but need $250,000 in pocket money next year.

- One year later, you sell $250,000 of the stock and realize a capital gain of $13,750. Most of the money you will spend is considered principal.

- Your tax rate is at or near 0% due to the 0% capital gains tax bracket, your standard deduction, or both.

- You have $10,300,000 left, keeping pace with inflation.

With $1,000,000 we are in good shape. There, we have $55,000 of upside, even more control over capital gains, and more. There are all kinds of tax things you can do at a lower income level, for example, you can avoid paying Social Security taxes if your income is low enough. There are many possibilities.

Over the long term, the tax code incentivizes you to invest in stocks and municipal bonds. If we rerun the above example with Nasdaq (QQQ), the tax implications would be more or less the same. The main difference is that investors have to deal with significant volatility and risk. However, BOXX is structured to help investors who want to wait out the current mania without being punished for it.

WHAT ARE THE RISKS WITH BOXX?

When I read the Bloomberg article, I started looking for risks, especially potential hidden risks. I didn’t find anything troublesome. BOXX reveals related risks In its prospectus, I encourage you to read it yourself. Most of these risks are boilerplate, and if you read enough you’ll understand which risks are relevant to a particular fund and which are not.

In any cash equivalent investment product, the main risk you should be aware of is counterparty risk. BOXX uses options in its strategies, where payments are guaranteed by the Option Clearing Corporation (OCC). OCC credit rating is AA It was included on the Federal Reserve’s list of institutions that are “too big to fail.” They had no payment problems during the 1987 crash, 2008 or COVID-19. I don’t think this risk is too serious. Money market funds also have counterparty risk, typically from commercial paper. The Fed implicitly supports all of this, but it’s worth knowing.

The second is not a risk per se, but box spreads are not needed in retirement accounts because they are already not taxed on current income. Money market funds work well there, so while you’re not losing anything by putting BOXX into a retirement account, you’re not really gaining anything either.

The third risk comes from execution. Box spread yields typically trade at a premium to Treasuries, but I think this premium could reverse if significant amounts of money flow into the strategy. Boxed spreads are a niche within a niche, so I don’t expect that to happen. If more high net worth money comes into the strategy, then I would expect tax-agnostic institutional money to exit – which should keep things balanced.

The fourth risk to be aware of relates to potential changes in taxation. I’m writing this in 2024, but Congress may change these rules in the future. Billionaires have been using boxed jam for decades, but who knows if ordinary people will ever tolerate eating the forbidden fruit. Also, it’s worth noting that funds will not explicitly commit to not distributing capital gains, but 99% or more of the time they will not do so in practice. If this risk materializes, we may still come out ahead as long as the favorable tax treatment remains in place.

After doing my due diligence and looking at the fund’s track record, I would feel comfortable putting a substantial amount of money into BOXX. If you are considering investing, you should conduct your own due diligence and consult your investment advisor, tax advisor, etc.

bottom line

BOXX currently offers a 5.5% return that is tax deferred and can be treated as long-term capital gains if you hold it for at least a year. This is a game changer for investors looking for low risk and long-term capital gains tax treatment. Based on these considerations, I named BOXX my top pick for 2024.