ipoba

investment thesis

simply put, Dynatrace Corporation (NYSE:DT) to detect problems, optimize performance, and minimize application downtime.

The bull case shows that Dynatrace is hugely profitable, with 5% of its market capitalization comprised of cash and No debt.

However, the bear case here suggests that its valuation does not provide a sufficient margin of safety. Having to pay about 31 times forward non-GAAP operating earnings already reflects many of Dynatrace’s very high expectations for next year.

Therefore, I downgrade DT to Hold.

quick review

Back in December, I ended my optimistic article by saying:

Given its stability and predictability, I don’t think investors will pay a large premium, and with free cash flow expected to increase in fiscal 2025, Dynatrace provides a reasonable entry point for potential investors.

Author’s work on DT

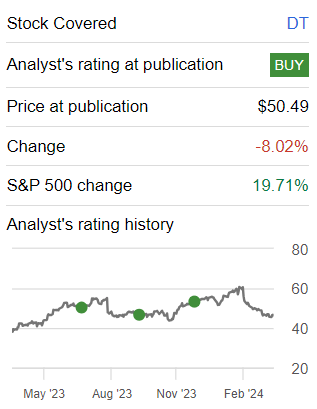

In hindsight, I made the wrong call on this stock as it significantly underperformed the S&P 500 (SP500). Simply put, I expect free cash flow to increase in fiscal 2025. But now I realize that my estimate was too high and inconsistent with the underlying reality of Dynatrace. So that’s why I’m downgrading this stock to Hold right now.

Dynatrace’s near-term future

Dynatrace provides software solutions to help enterprises monitor and optimize their digital operations. Essentially, they provide tools that allow companies to keep tabs on how their applications are performing. Dynatrace’s platform uses advanced analytics to detect issues and identify areas for improvement to keep everything running smoothly.

With a strong pipeline and growing interest in trading larger strategies, Dynatrace expects to capitalize on the opportunities presented by the growing demand for automated observability and application security solutions.

The company’s investments in target market segments and R&D innovation, including its recent acquisition of Runecast, explain why its underlying earnings guidance isn’t as strong as many had hoped (more on that soon).

The launch of new solutions such as Dynatrace AI Observability and Dynatrace OpenPipeline further enhances the capabilities of the platform, providing customers with insights into AI-driven applications and giving them complete control over data management.

Despite its promising prospects, Dynatrace has had to rethink how to balance growth and profitability, particularly with its public investments.

With this background, let’s take a deeper look at its financials.

Will grow at a CAGR of 22% in the upcoming fiscal year

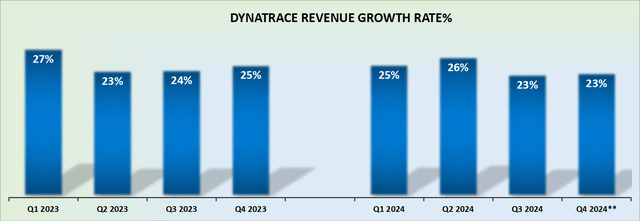

DT revenue growth rate

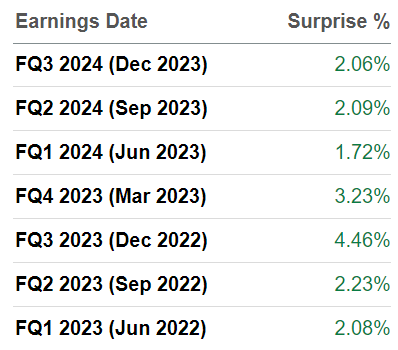

When Dynatrace reported its fiscal third-quarter 2024 results and guidance, it didn’t significantly raise its fiscal fourth-quarter guidance. However, as most quality companies do, Dynatrace will likely lower its guidance by a few percentage points to allow for a slight beat on estimates when it reports. Along those lines, see how recent seasons have fared below.

AT Premium

With this in mind, I’m increasing management’s guidance by 3%, bringing it to 23% growth in the fiscal fourth quarter.

Therefore, as I plan for fiscal 2025, which begins next calendar month, I expect Dynatrace to grow approximately 20% next year. It could end up growing a few percentage points faster than that, but considering its current ARR is growing at 21% annualized in constant currency, I find it hard to imagine it growing anywhere near the same rate as roughly 20%-22%. significant difference. Therefore, I assume Dynatrace will grow at a CAGR of 22% next year.

Next, we’ll discuss its valuation.

DT Stock Valuation — 31x Forward Non-GAAP Operating Earnings

For the final nine months of fiscal 2024, Dynatrace’s non-GAAP operating margin was 29%.

However, Dynatrace expects non-GAAP operating margins in the fourth fiscal quarter of 2024 to be around 23% to 24%. Even if we assume management plays conservatively when it actually reports fourth-quarter financial results to beat easily, and that its non-GAAP operating margin actually hits 25%, that would still leave Dynatrace trailing nine months into the year relative to the rest of the year.

Beyond that, if we compare to Dynatrace’s prior year, it reported a non-GAAP operating margin of 25%. Therefore, I believe that all of Dynatrace’s efforts to increase its potential profitability may have reached its limit and been eliminated.

With this in mind, as we look to fiscal 2025, we assume Dynatrace’s underlying profitability expands a further 200 basis points from this fiscal year. This will bring Dynatrace’s non-GAAP operating margin to 27%, meaning that in the short term, Dynatrace’s profitability will be comparable to Dynatrace’s operating capabilities.

As a result, non-GAAP operating profit of approximately $460 million was as good as expected for the coming year. So all the likely benefit to investors in the coming year is an increase in underlying profitability of about 10% to 15%.

Does paying 31 times forward non-GAAP operating profits really make sense, given the backdrop of 15% underlying profitability growth?

Even if I’m wrong and Dynatrace is more profitable and approaching $490 million in non-GAAP operating profits, that would give Dynatrace a multiple of 29 times forward non-GAAP profits. While the latter’s valuation is clearly more favorable than the former’s, it means investors will have to expect a very optimistic scenario to match the expected price. All in all, I’m not that optimistic at all.

bottom line

Overall, when I look at Dynatrace, Inc.’s near-term prospects, I see challenges to its valuation.

For example, its underlying profit guidance wasn’t as strong as many investors had hoped. Despite having a solid product pipeline and strategic investments in R&D, Dynatrace faces challenges in striking the right balance between growth and profitability.

Looking at its financial position, it is expected to have a CAGR of 22% in the next fiscal year. However, given the valuation of 31x forward non-GAAP operating earnings, I find the margin of safety insufficient. As I approach this scenario, I have to weigh the potential upside against the expectations that are already priced in, which leads me to take a more cautious stance on Dynatrace’s near-term prospects.