One of the most common questions I get asked is what to do when an investor receives a large amount of cash, perhaps from an inheritance or the sale of a business. Should they invest it all at once or average cost (DCA)? Fortunately, empirical findings provide the best answer from a purely financial perspective.

Academic research, including the 1979 study A note on the suboptimality of the dollar–Cost averaging as an investment policy, 1992 study No one benefits from dollar-cost averaging: Analytical, numerical and empirical results, and the 2011 study Does dollar-cost averaging make sense for investors?, The study found that investors’ odds of winning improved significantly if they invested in all assets at once – and that when DCA performed well (in a few cases), it tended to perform better than when it performed poorly (in most cases) Much less.

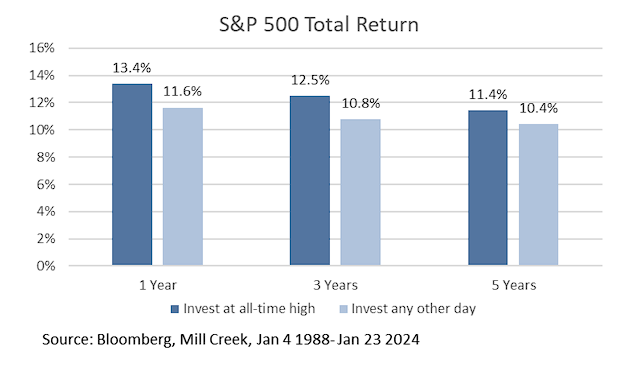

When I present this evidence to investors, I’m asked, “While the average is true, the market just hit an all-time high, so maybe I should wait for a market pullback?” Thanks to Principal at Mill Creek Capital Advisors With help from Chief Investment Officer Michael Crook, we can put the evidence to the test evidence. Crook looked back at the S&P 500’s returns in the one-, three- and five-year periods following its all-time high and compared them to the returns of purchases on any other date. His data sample covers January 4, 1988, to January 23, 2024. As the table below shows, buying when the S&P 500 was at all-time highs outperformed buying on any other date during each holding period studied, with outperformance ranging from 1 percentage point to 1.8 percentage points.

Despite the empirical evidence, DCA remains a popular strategy among individual investors. The strategy’s popularity stems, at least in part, from our lack of understanding of the evidence under review. DCA is a risk-averse strategy that has also proven its popularity, as those adopting the strategy hold on to cash until the plan is fully implemented. Furthermore, behavioral scientists would explain that DCA investors are popular because they try to minimize the potential regret (loss aversion) of one-time investing.

Important points for investors

Historical evidence clearly shows that DCA is a poor investment strategy. That said, it may still serve a purpose: if you’re very risk-averse, you won’t invest if you’re forced to choose between investing a lump sum or not investing at all, then DCA becomes a “two evils” The right should be taken lightly.”

Larry Swedroe is director of financial and economic research at Buckingham Strategy Wealth, LLC and Buckingham Strategy Partners, LLC.

Provided for informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is based on third-party data and may be outdated or superseded without prior notice. Third-party information is deemed reliable, but its accuracy and completeness cannot be guaranteed. The views expressed here are his own and may not accurately reflect the views of Buckingham Strategic Wealth LLC or Buckingham Strategic Partners LLC (collectively, Buckingham Wealth Partners). Neither the U.S. Securities and Exchange Commission (SEC) nor any other federal or state agency approved, determined the accuracy, or confirmed the adequacy of this article. LSR-23-617