Sergio 74

Above: Macau’s growth rate is ahead of many early calls for recovery.

We accept what some investors have described as our bullish outlook Las Vegas Sands (NYSE:LVS) last year as A Faded Broken Record This is understandable considering the stock is facing significant resistance near my price target (“PT”) of $70. The stock even struggles to get above $50. Mr. Market’s collective shrug continues to confuse many stock fans, myself included, given the strong performance we’re now seeing from the company in post-COVID Asian markets. The recent FY23 results could be a very good start,

I’ve taken a deep dive into this stock several times over the past few years.I added gaming career-based insights that generally go beyond most standard analyses. stock. I thought at one point that I didn’t realize the consistent investor secret, “Falling in love with a stock often leads to investor abandonment.” I got it, but continuing my positive attitude would still win out. I will use my best instincts and knowledge from 35 years in the casino business to take on Mr. Market.

Google

In previous Seeking Alpha posts, we attempted to put together a set of factors, any one of which could lead to continued suspicion. We, like many holders, are wondering whether the capital structure, with a 50% stake in the hands of Sheldon Adelson’s widow and foundation, will deter investors. Or whether the recovery in Macau and Singapore’s gaming markets so far has not yet reached a point of comfort for non-believers. And lingering on the left is the perceived vulnerability that mainland China’s growing anti-American saber-rattling, coupled with its weak economy, poses the greatest threat to the entire industry.

Google

Above: There is a core group of investors who are wary of companies like LVS because their entire business relies on the goodwill of dictators. We understand this, but our long experience in the Asian gambling industry shows that this is not the case and the Chinese never leave a penny on the table. The renewal of Macau’s gaming license tells a more optimistic story.

LVS continues to be bullish in 2023, with 2024 Asian gaming prospects accelerating towards full pre-pandemic recovery territory

LVS revenue performance in fiscal year 2023:

- Revenue: $10.4b, up 152% year-on-year (2022 still partly affected by COVID-19 disruption, with air travel schedules remaining below pre-COVID arrivals).

- Net profit: Loss ($1.07b) increased by $1.22b from 2022.

- Profit margin: 12% increase from net loss in 2022.

- EPS: Up $1.62 in 2022, loss ($1.40)

- P/E vs. Peers – LVS Price at time of writing: $54.50

- LVS: 31.98

- Wynn: 168.5

- MGM: 40. (ttm)

- Czech Republic: 46.30

- MLCO: 27.86

- Market share increased: LVS performance levels for FY23 include revised estimates of Macau market share from bank and official sources. LVS delivered the largest gain in market share this year.

LVS’s share increased from 23.4% in February to 26.1% in February. Overall growth was 3.2% and continued to rise in mid-24 months.

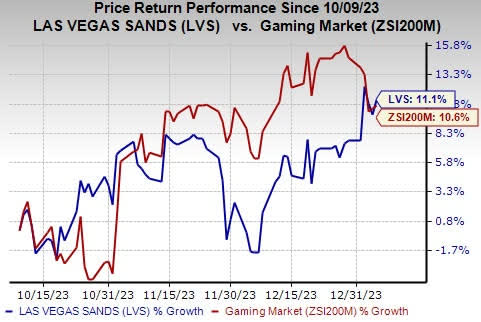

Our buy call on September 20, 2023 – The stock price that day was: $48.38, but clearly still unable to stay above $50 for the long term.

January 28th This year, our call options on Seeking Alpha have the stock priced at $50. As of today, major analysts have a PT of $63 and a Hold rating.

After reviewing LVS data and the forward market outlook for Singapore and Macau, we continue to buy with an unchanged price target of $70 by the end of Q2 2024.

Of course, the huge year-on-year shift in LVS is directly related to the strong recovery in Macau and Singapore.

Fitch currently expects gaming revenue in the Macau market to reach 80% of the 2019 baseline due to a 15% year-on-year increase from 2019. This means the six franchises will receive $2.66 billion in gaming revenue. If LVS maintains market share, it will earn $675 million in gaming revenue. In the first quarter of 2024 alone, sales in Macau are expected to reach $7.15b, an annual increase of $65b. These figures illustrate what we have long believed to be the eternal reality for Asian gaming customers:

Unless macro events are catastrophic like the COVID-19 epidemic, China’s GDP decline will not actually stop regardless of cyclical economic difficulties.

Arrivals increase bull case scenario

Macau officials expect the total number of tourists to Macau to reach 33 million in 2024, an annual increase of 17%, reaching more than 80% of the 2029 baseline.

Singapore’s tourism agency expects to receive 16 million tourists, 18% of which originate from mainland China. Until last year, Singapore’s number one starting point for tourism was Indonesia.

In Macau, LVS benefits from its 12,000-room capacity and coverage of various consumer segments from modest to high-end room rates, dining and entertainment facilities. Likewise, Marina Bay Sands and Genting are in a duopoly position.

(notes: Investors have long had questions about the status of a planned fourth tower at MBS Properties. We’ve checked with Singapore’s best sources. They told us that the country’s Urban Redevelopment Authority has approved the MBS expansion this month and it will be launched next month (April). The $330 million project will have 587 rooms, down from the 1,000 rooms originally planned. )

Investors have been questioning whether the project’s reduced size reflects LVS’s concerns about the long-term prospects of the Singapore market. Our sources believe the downsizing reflects a post-pandemic “simple prudent investment review and they may consider a two-stage process.”

Goldman Sachs picks 25 opportunity stocks: LVS is one of them

In a recent report, Goldman Sachs selected the 25 stocks it analyzed that had the highest dispersion scores, meaning stocks that showed a high degree of dispersion relative to a benchmark hot stock. Ratings range from above 8 to around 6. LVS ranked 19th. For context, United Airlines Holdings (UAL) is ranked 6.8, Advanced Micro Devices (AMD) is ranked 6.1, and LVS is ranked 6.8.The overall guidance on the checklist is catch. We cite this report primarily because it suggests that the stock may be bullishly mispriced, and this information comes from algorithms that have proven to be correct at a high rate over time.

We note that transfer testing is not necessarily conclusive, as is the case with many of the formulaic data sets we see every day. Nor are algorithmic analysts hanging around in the background with occasional thumb twiddling. However, we believe that the fiscal year results and forward-looking bullish tone in the Macau and Singapore markets, combined with LVS’ control of market share, tell us that the $53 stock is worth holding.

in conclusion

We think there’s still more to like about LVS than there is to be wary of. At the current trading price, it seems quite reasonably priced. To us, however, this does not entirely reflect a sustained catalyst, but rather a continued cautious northward movement. The margin of safety is clearly appropriate for worst-case scenarios (excluding black swans of course).

Two sources put LVS’s intrinsic value at $54.75, which is where it’s currently trading. I think these five-year estimates still reflect some overly conservative FCF forecasts for COVID-19-affected quarters.

So, we set off again with $70 in PT. Commenters who disagree are welcome to question my bull market scenario. I can be persuaded by tough arguments, but keep in mind that I have invested over 35 years in the casino industry and I admit that bias does occur in the long run.