Michael Way

Palantir investment thesis

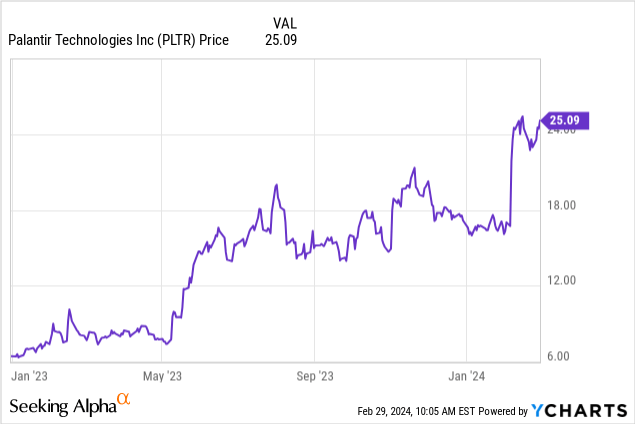

Palantir Technologies (NYSE:PLTR) last year coincided with the launch of Palantir AIP.The stock benefited greatly from this and performed very well So far. The introduction of bootcamps to help potential customers understand how to apply artificial intelligence and see use cases was also a great success. In particular, operating systems can now be set up in days instead of months, which contributes significantly to success.

But the market is currently pricing in a very high growth rate, and I think this also shows that this is a very high-quality company in the eyes of market participants.The key now is to figure out whether the market still underestimates Palantir’s chances of seeing the light of day future. So let’s take a closer look at the company.

What exactly does Palantir do? How do they aim to provide customer value?

Palantir was founded in 2003 to participate in the counter-terrorism industry. As a result, over the years, most of its clients have been government agencies. But the structure has changed, with 55% of customers in fiscal 2023 being government and 45% commercial. The remaining deal value is $2.1 billion for the commercial side and $1.8 billion for the government side, so the commercial side will likely be the larger of the two going forward.

Palantir currently consists of 4 different platforms. A major turning point is the launch of AIP in 2023, which uses machine learning and LLM alongside data from other platforms.

Gotham and Foundry, on the other hand, act as operating systems, reflecting the data being manipulated and helping users identify patterns in data sets as quickly and easily as possible. That’s because Palantir is committed to ensuring users can get the most out of the platform, regardless of their level of technical expertise.

The resulting platform, Apollo, is a single layer of control that orchestrates everyone’s access to the latest updates and features, whether they’re in the cloud or elsewhere working with Palantir.

Does PLTR have a competitive advantage and are there any barriers to entry?

The barriers to entry are very high. On the one hand, the installation cost is high, and on the other hand, the data environment is very complex. Additionally, Palantir is rooted in collaboration with intelligence agencies, which ensures the highest level of data security.

also, Palantir’s Virtual Desk will make it easier for customers to begin what is often a very complex process. Palantir’s goal is not to replace what’s out there, but to use them as a layer that connects data to models and the real world, so customers don’t have to copy data, as Palantir is compatible with AWS S3 (AMZN), Snowflake (SNOW) , BigQuery (GOOGL) and Azure (MSFT).

Beyond that, Palantir customers don’t need to know how machine learning or artificial intelligence works, but can still use the results. For example, AIP logic Allows unit testing and debugging without writing new code, and AIP scenarios show the possible effects of operations. In addition, AIP Automate can also automate certain processes on this basis.

Palantir works hard to make the transition as easy as possible for customers.and SDDI or software-defined data integration, expensive and time-consuming manual customization of the semantic layer is no longer required. And no new lines of code need to be written.

So Palantir brings analytics, workflow, integration, data, and AI/modeling all in one place. Easily and securely synchronize with existing ERP, MES, and SCM.

If these models prove to be more accurate and faster than current solutions in predicting trends in the future, there will be a huge competitive advantage. By then, I believe Palantir will become mission critical to its customers, who will become more dependent on it the longer they use the platform. Then the cost of switching would be immeasurable.

Real-life examples of how organizations benefit from Palantir software

Corporate marketing departments often throw out buzzwords, so I thought it would be a good idea to look at real use cases to see if Palantir actually creates value for customers.

For example, Palantir’s Hospital Solutions The staffing ratio of nursing staff increased by 30%, and the length of stay of patients in the anesthesia department was shortened by 28%. Clearly, these two examples create value for both customers and the business.

Ferrari (RACE) has been a Palantir partner since 2017. Benefit from being able to detect anomalies faster and more efficiently, allowing them to spend more time analyzing data instead of collecting, organizing, and cleaning it. Anyone who has used Python or other languages knows how much time it takes to clean and organize stuff. in the past, As much as 80% of time is spent on these tasksand the actual analysis time is much less than most people imagine.

Palantir helps Swiss RE (OTCPK: SSREY), one of the world’s largest reinsurers Significantly reduce the time required to generate reports. Reinsurance is a very complex business that ideally requires instantaneous analysis of data while adhering to strict regulatory privacy guidelines.

Fujitsu (OTCPK:FJTSF) Chooses Palantir Optimize its supply chain and modernizing its technical infrastructure. The partnership comes as Fujitsu CEO Takahito Tokita says Palantir’s track record of solving complex problems is important.

I think it’s great to see some big companies looking at Palantir as one of the best partners for solving complex problems because their models may be ahead of their competition in terms of identifying trends or predicting trends more accurately. Another thing Palantir does well is They manage to get many different users using different systems to work perfectly together to save time. Every time you save time, you save money.

PLTR’s Balance Sheet and Indicators

Palantir Q4 Earnings Report

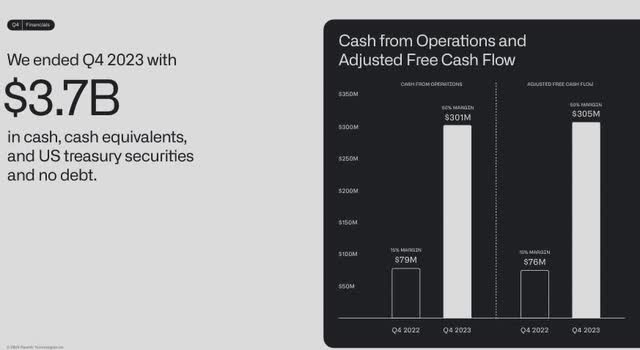

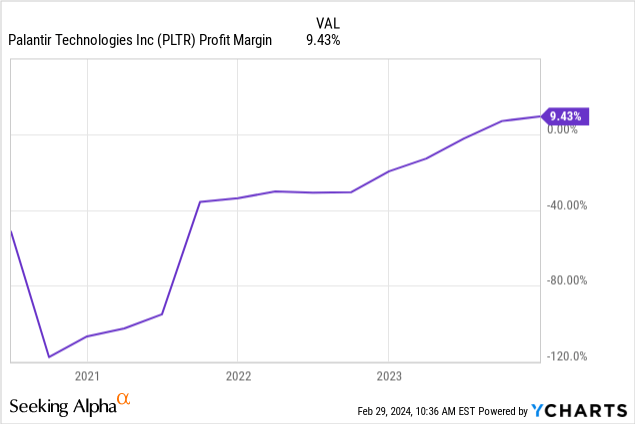

With $3.7 billion in cash and no debt, Palantir is in excellent financial shape. Additionally, since the company has positive free cash flow and positive net income, it will have enough money to invest in growth opportunities in the future or return capital to shareholders at some point.

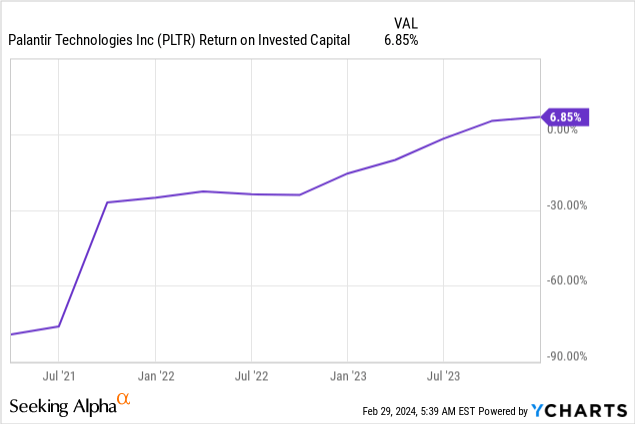

Currently, ROIC is below average, but is increasing, and Professor Mauboussin’s research Research shows that companies that improve their ROI are among the best performing companies. Since Palantir hasn’t been profitable in a long time, I think we’ll see significant earnings growth in the next few quarters.

Palantir Q4 23 earnings report

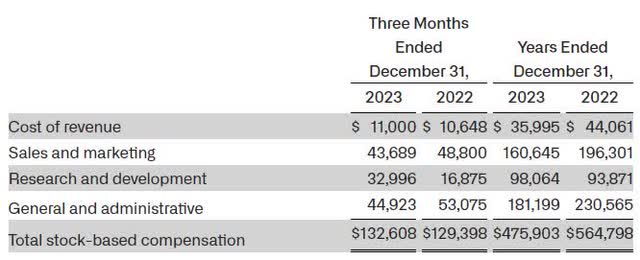

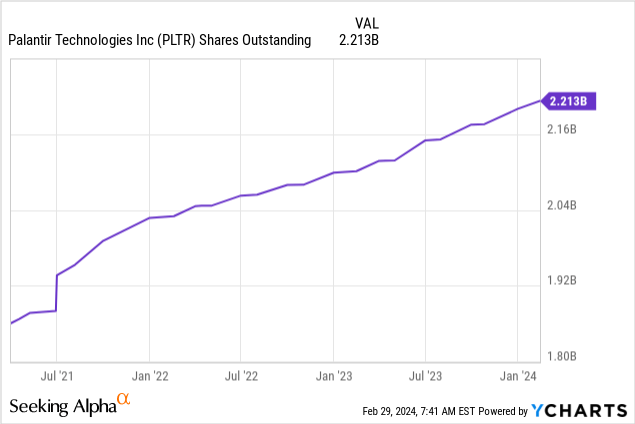

Fortunately, the number of SBCs in Palantir is also decreasing. SBC costs were $564 million in fiscal year 2022, compared with only $475 million in fiscal year 2023.

However, the new share issuance creates a higher level of dilution, but if earnings per share continue to rise in the next few years, that will be fine. However, a flat or declining share float would be a better bet going forward.

Is Palantir having too much inside sales?

I think most people interested in Palantir right now are following the discussion about insider sales, In particular, CEO Alexander Karp’s stock sell-off. Palantir’s inventory situation is a little more complicated than other companies. It’s more common for companies to have A and B shares with different voting rights, but Palantir also has F shares, This effectively gave the founders at least 49.99% of the vote.

Therefore, no matter how many shares they sell, they are likely guaranteed to always have a majority of the voting power along with the F shares. However, Thiel owns Class A shares, accounting for about 7%, lower than the founders of most other well-known companies. For example, Zuckerberg owns 13% of Class A Meta shares and Musk owns 20.5% of Tesla. So it’s safe to say that the other founders have a bigger slice of their companies’ pie, but Thiel and Karp’s interests are still aligned with those of shareholders, as their stakes still run into the billions.

Palantir is valued via inverse DCF

author

The market’s expectations for Palantir are very high. Currently, the market is pricing in a 10-year compound growth rate of diluted earnings per share of 40%. But it’s also because diluted earnings per share of $0.09 is a very small starting point. So for the stock to be fairly valued, earnings per share would have to be around $2.60 in 10 years, which I think is pretty realistic.

Palantir Q4 23 earnings report

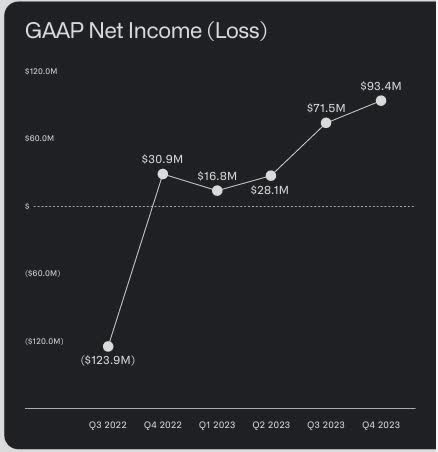

Within a year, Palantir’s net income tripled, from $30.9 million to $93.4 million. Therefore, I expect growth to continue to be strong in the coming quarters. If they can grow and be profitable at the same time, they will create tremendous shareholder value.

Where will EPS go in the future?

Seeking Alpha Profit Predictions

Profit forecasts from 17 analysts are that by the end of 2024, earnings per share will be 3.5 times current earnings per share. Then from 2024 to 2025, the growth is only 18%, which I personally think is too low. I think earnings growth is undervalued and Palantir will outperform analysts’ expectations.

I strongly suspect that revenue and net margin will increase over the next five years. I wouldn’t be surprised if we see earnings of $1 per share by the end of 2027. At a P/E ratio of 40 to 50 times, if Palantir’s earnings hit $1 per share, its stock price would be $40 to $50.

But Palantir is likely a long-term hold, with its true value taking 5 to 10 years to emerge. In the short term, the stock could move wildly.

Risks to Palantir’s Business

The most obvious risk may be that Palantir’s predictions are inaccurate, and since we may only be in the first inning of the AI era, a lot can happen and innovation happens quickly.

Since we are still in the early stages, laws and regulations may change significantly.It will be interesting to see the impact CCPA and CPRA. Ethical issues may also become more important.

In addition, the fact that the three largest customers account for 19% of total revenue is a cluster risk. But I think the biggest risk is probably in the area of cybersecurity. AWS and Azure host some platform functions, so cyberattacks can be a big problem. Especially since the data used is very sensitive and potentially very important.

in conclusion

Palantir has extremely high barriers to entry, benefits from high switching costs, and is expected to build a significant competitive advantage through its model. In the future, Palantir’s best-forward scenarios and models may become standards across industries. If they succeed, the benefits could be huge.

Inclusion in the S&P 500 may help the stock in the short term, but in the long term, earnings per share and its performance are what matters most.

However, with margins and return on invested capital trending upward, and revenue trending higher, I expect diluted EPS to surprise the market. In 5 to 10 years, Palantir will likely be in much better shape than it is now.

If they buy back shares at some point to significantly reduce the number of shares outstanding, this will have a very positive impact on earnings per share. I certainly hope FCF can be strong enough to return capital to shareholders over the next few years.