Simalik

From 2010 to 2020, the merger arbitrage strategy was an excellent alpha generator. The U.S. government quickly approved most mergers, creating low-risk, high-profit opportunities for merger arbitrage strategy ETFs such as the IQ Merger Arbitrage ETF (NYSE:MNA).since The strategy of merger arbitrage failed to materialize after the new administration came into power, and ETF MNA has been declining since 2020, while almost all equity funds are rising. In my opinion, the next few months will be exciting for buyout funds to watch to see how U.S. government politics will impact Generation Alpha of this strategy.

First, I must state that my views on MNAs are not political. However, we cannot shy away from the political element when discussing niche markets, as the FTC’s executive branch policies are largely politically motivated.The core reason for Fund MNA’s weak performance is Biden The administration may be the most antitrust it has been in decades, blocking a number of large mergers in recent years.

Crucially, this is not a statement of political opinion, because for me, blocking the merger has both positive and negative consequences. That is to say, Biden’s administration has Blocked more mergers than Obama and twice as many as Trump. Unlike the Trump administration, Biden is more focused on horizontal mergers than vertical mergers, which are more important for MNAs.

Looking ahead to an election year, now is a good time to pay closer attention to ETF MNA. Overall, I expect this ETF to underperform in 2024; however, stagnation is more likely than losses. Looking ahead to 2025, the Biden administration may change priorities due to economic needs, or the Trump administration may allow more mergers, which could improve MNA’s performance. That said, investors weren’t necessarily expecting returns from the massive M&A environment of the 2010s.

FTC Policy and the Boom and Bust of MNAs

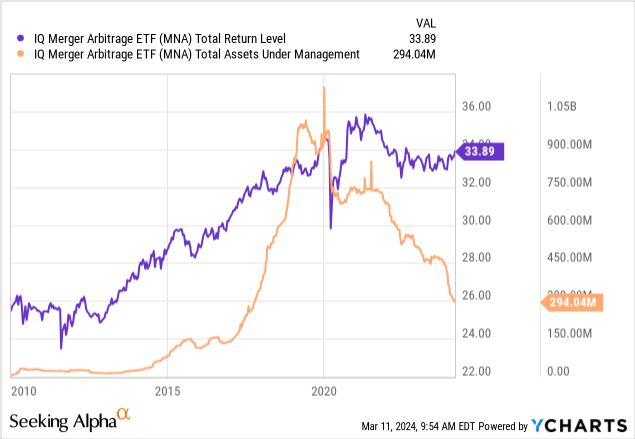

ETF MNA was once relatively popular, with total assets under management of just over $1 billion, peaking in 2019. Its good performance continued into 2020, despite a sharp short-term decline that year as lockdowns occurred and increased trading volatility. The company has been stagnant since 2021, losing little in overall value and seeing its AUM drop by nearly 80% as its performance significantly underperformed its peers. See below:

In short, MNA is not a popular approach today. Few investors pay attention to it, and it gets less analysis than most. Personally, I find under-covered stocks and ETFs interesting because there is less media attention and market volume, and the markets tend to be less efficient. Of course, the media focuses on merger activity and its lack thereof, but less so on the merger arbitrage strategy, which has fallen by the wayside since the Biden administration changed the FTC’s approach.

Fundamentally, despite ETF MNA’s underperformance, there are many reasons to be bullish on it. MNA earns revenue by purchasing shares on public takeover announcements. Typically, stocks in merger transactions move very little from day to day. When a merger is announced, the shares typically trade a few percentage points below the merger price to adjust for the risk of the deal falling through.

MNA acts as a liquidity risk provider for consolidated transactions.Therefore, it will benefit from an increased success rate of merger transactions or Discount on combined transactions increased. The latter is critical as merger deals are increasingly discounted and adjusted for the possibility of an FTC blockade. As an example, one of MNA’s broader holdings is Discover Financial (DFS), which was purchased for $35B but currently trades down more than 13% due to FTC exposure.Additionally, DFS is currently trading just $10 (or 9%) above its pre-merger price, which could limit its downside risk if the FTC blocks it – i.e. controversial Political and financial fields.

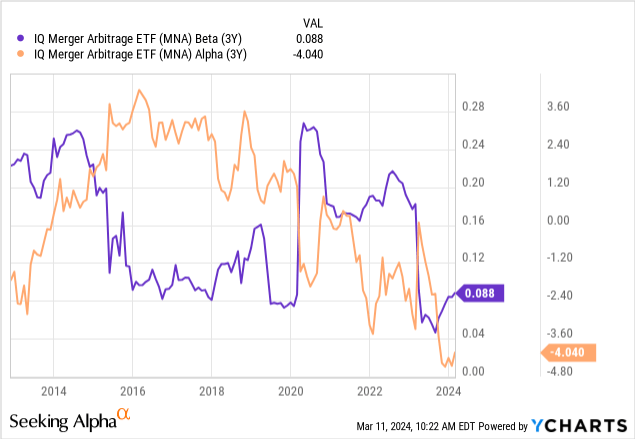

Because MNA is focused on arbitrage, it has less correlation with broader stocks, making it historical Alpha generator. It had a very low beta of about 0.09x against the S&P 500, never exceeding 0.25x, while its alpha was about 3x during the peak of the 2015-2018 consolidation period. See below:

MNA would be a valuable fund were it not for the poor external environment. The key to long-term wealth creation in financial markets has less to do with short-term performance and more to do with managing value at risk.Historically, MNA has had very low correlation with the broader equity market and generally has lower overall volatility Annualized 5.3% Past 200 days vs. 11.8% S&P 500 Index. While its strategy hasn’t performed well recently, it was an extremely diversified alpha generator prior to 2020. In my opinion, investors shouldn’t be quick to sell it because of its positive long-term returns and, most importantly, its tremendous diversification value.Because of its lower beta, it should reduce overall portfolio volatility while also ideally Provides positive returns above interest rates.

Merger Arbitrage – Profit Outlook 2024

This is a global fund, Approximately 40% of shares held Therefore, for some MNAs, the FTC’s anti-merger stance does not matter.In other words, most antitrust activities in the United States are also found in europe. Since 2020, the increase in the cost of living has greatly promoted people’s inflationary mentality, and they are more concerned about lower prices. As someone who analyzes companies, I would say that outside of the largest 100 companies, most companies are also losing out to inflation, with consumer prices not rising as fast as costs.That said, most U.S. consumers won’t necessarily understand this perspective, with many pointing out corporate greed as a cause of inflation.Therefore, as long as global consumers are low personal savings In this environment, I expect antitrust sentiment to maintain or grow.

While the Biden administration’s role in the FTC strategy is notable, this is an increasingly global phenomenon. It’s worth noting that antitrust and antitrust sentiment is on the rise and is largely one of the few bipartisan perspectives.More than 80% of U.S. Democrats support antitrust lawand 62% of Republicans. Independents have the lowest approval rating at 60%, but still hold a majority. Entering an election year, no one will win votes by openly supporting a merger campaign, which could hinder the MNA’s potential no matter who wins in November.

That said, I am not bearish on MNA today. While I don’t expect the FTC or similar agencies around the world to allow more broader mergers, MNAs may benefit from greater risk-adjusted discounts on merger deals than in the past. Before the M&A crackdown intensified in 2022, shares in many M&A deals were trading very close to the acquisition price, making M&A arbitrage a lower-reward and higher-risk proposition.

Today, discounts have increased. However, precise quantification is not easy. MNA’s largest holding is WestRock (WRK), with about 6%. WRK is expected to be acquired by Smurfit Kappa ( OTCPK:SMFTF ) for a price of SMFTF plus $5, or $47.91, or about a 6% premium to WRK’s current price. This is a lower discount because the FTC is less likely to block the deal; however, investors should research the exact pricing of the deal as it may differ from mine.

MNA’s second largest holding is Karuna Therapeutics (KRTX), trading at $319, Purchase price $330, making it up about 3.5% today.Next up is U.S. Steel (X), which $55 off, currently trading at $47.5, offers a solid upside opportunity of approximately 16%.Then, we have Pioneer Natural Resources (PXD), my long-term bullish stock, trading at $242 versus Purchase price $253bringing it up 4.5%.

Again, this metric is not widely measured, but in most cases I believe we see larger discounts on mergers due to the increased risk adjustment. Therefore, as long as we assume that deal failure rates remain consistent, MNEs should start to make some headway as the advantages of mergers and acquisitions are more pronounced. MNA does have a higher expense ratio at 77 basis points, but to me that’s relatively fair given its low beta relative to the S&P 500 and its long history and potential for decent returns.

bottom line

Overall, I am slightly bullish on MNA today. There are three reasons behind my opinion. First, MNAs are purchasing merger deals at seemingly larger discounts to acquisition prices, offsetting higher deal failure rates. Second, MNA has very low market correlation, so these potentially positive returns are a great way to reduce portfolio volatility by focusing on alpha generation.

Finally, I believe there is a good chance that M&A deals will be more successful in the coming year than in the past two years. One of the big deals that fell through recently was JetBlue Airways (JBLU) and Spirit Airlines (SAVE).As detailed in my recent article, I believe one or both Without the merger, the airlines are likely to fail. Therefore, I believe the FTC’s decision could lead to massive worker layoffs, which could lead the Biden administration to abandon its strong antitrust policies.The other one, Capital One (COF) and Discovery, I expect will not blocked Because both banks are financially weak, there are risks faced by regional banks; therefore, the merger should reduce risks in the banking industry.

Historically, a Trump victory has been a boon for MNAs, as his administration has allowed many mergers to proceed. Still, even with Biden, I think the odds of merger success will likely increase because of the economic needs of many companies. We are seeing many merger deals between risky companies that are losing profits to inflation. While lower profit margins are good for consumers, a significant drop in corporate profit margins can lead to layoffs. One could argue that the Biden administration will do more to stem unemployment than inflation. In today’s context, I think mergers protect jobs (especially blue-collar workers, as opposed to accountants, managers, etc. – who are often fired in mergers), although likely to increase inflation.

My latter view is speculative and depends on November and the government’s response to the possible imminent collapse of Spirit Airlines. That said, increased government approval of mergers would be very bullish for MNAs since the discounts on deals currently being challenged by the FTC are so high. No one will get rich investing in MNA, but the potential for positive returns without high market correlation makes it a good ETF to put 3-10% of your portfolio into.