dmitriymoroz/iStock via Getty Images

summary

Sonoco Products, Inc. (NYSE:SON) focuses on global sustainable packaging products, and its business is divided into three parts. Consumer goods packaging, industrial paper packaging, etc. Historical revenue growth has been increasing year over year, but ended with negative growth in 2023.Still, profit margins have been falling 2022 and 2023 will be strong. The paper-plastic packaging products and materials industry is largely affected by continued inflation and destocking. But in the long term, we can expect the industry to benefit from demand for sustainable packaging and expanding e-commerce activity. My conservative relative valuation model gives me modest upside potential of 7%, but lacks an adequate margin of safety. Therefore, I recommend a Hold rating.

Historical financial analysis

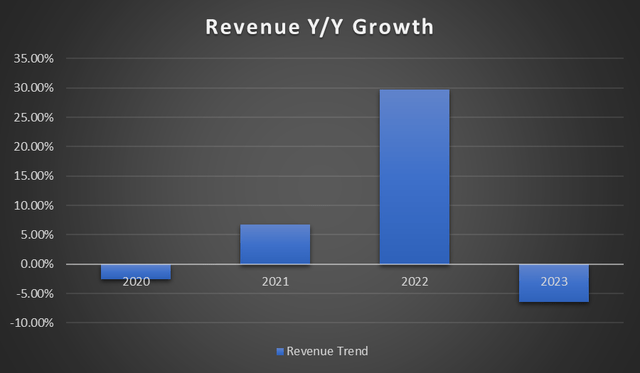

Revenue growth trended upward over the past four years but ended in decline in 2023.Decreased Annual growth of 6.47% in 2023 was primarily due to lower sales, although this was partially offset by acquisition revenue. Net sales increased 30% year over year in 2022 due to strong performance and the accretive impact of metal packaging acquisitions, although this was partially offset by lower volumes in the industrial segment.

Author’s chart

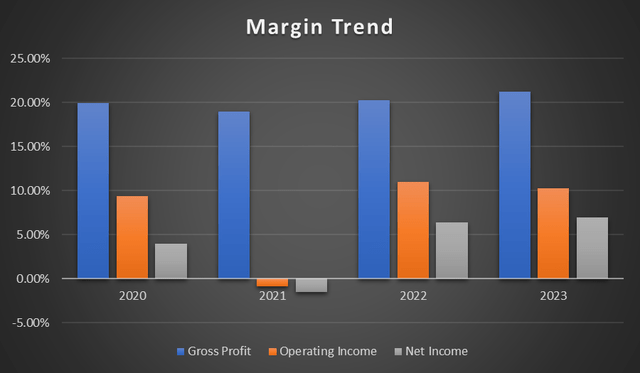

In terms of profitability, over the years, except 2021. The main reasons for negative net profit and operating income in 2021 are its pension settlement expenses and after-tax losses when paying off debt early. After 2022 and 2023, its profit margins have recovered and are slightly higher than 2020 levels. Overall, SON’s full-year margins remained strong despite fluctuations in revenue growth.

Author’s chart

Segment Overview

Author’s chart

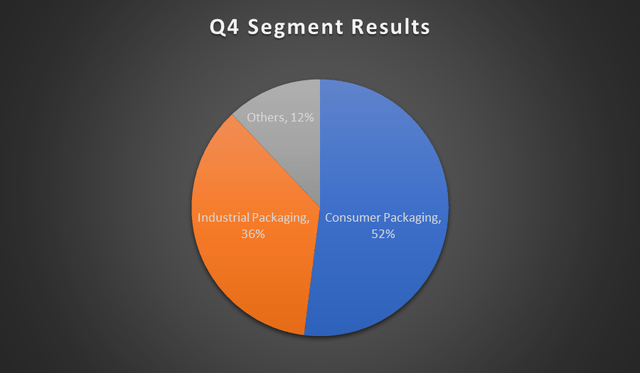

Consumer packaging segment market share 52% Fourth quarter net sales; 36% were from industrial packaging and the remaining 12% were other. As of December 2023, the Consumer Packaging segment consisted of approximately 80 plants worldwide. Its products include rigid and flexible packaging, primarily targeting the consumer staples market, with a focus on food, beverages, household and personal products. Rigid packaging (paper, plastic and metal) consists of thermoformed plastic trays and shells and is used primarily for fresh produce, pre-packaged foods and condiments. Flexible packaging is mainly plastic packaging for food and personal products. In 2023, its cardboard containers were the company’s largest revenue-generating category, accounting for 21% of year-end net sales. Industrial paper packaging, on the other hand, serves its market through approximately 190 factories spread across five continents. Their products include cardboard tubes, cores, reels, spools, uncoated recycled cardboard and more. They serve multiple end markets, including consumer staples, consumer discretionary and industrials. Tube and core products ranked second among the largest revenue-generating product categories, accounting for approximately 19% of its year-end net sales.

Segment Results for 4Q23 and Outlook for 2024

Net sales of consumer packaged goods decline 3% Season 4 of 2023 compared to Season 4 of 2022. Sales continued to be affected as consumers purchased less food and household goods as retail prices rose. The company attributed the sales decline to a year of customer retail destocking. In terms of operating margin, it was flat year over year as lower sales were offset by pricing initiatives.

For industrial packaging, net sales decreased 1% annually in 4Q23. The segment’s weak performance can be attributed to weak demand, lower pricing and unfavorable sales/mix. Operating profit fell 3% to 10% from 13% in the previous period due to low volumes and price/cost pressure.

For 2024, management expects sales to continue to be flat in the first quarter and expects low-single-digit growth for the full year as consumer spending declines due to retail price inflation. Industrial segment sales are expected to see a limited recovery due to rising input costs and ongoing challenges posed by index-based pricing.On the bright side, Fitch Ratings expects the index to trend downward price Prices of raw materials such as plastic resins, metals and other key materials have fallen from highs. This could at least improve SON’s profit margins.

Lingering inflation and destocking

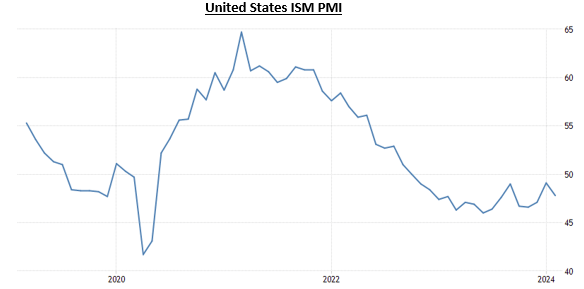

While destocking typically begins during COVID-19 supply chain disruptions, the issue continued to impact the industry in 2023 and was evident in both SON’s consumer and industrial segments. As consumer demand slows due to inflationary pressures, customers continue to manage existing inventories more closely, impacting packaging sales. Most companies expected destocking to wind down, but the effects lasted longer than expected. Even though we expect sales to improve slightly in 2024 as companies clear much of their inventory backlog, we still need to remain cautious as weak consumer demand amid high costs from inflationary pressures could still cause problems.expected Real consumer spending growth It will drop from 2.2% in 2023 to 1.8% in 2024 and 1.6% in 2025.The same is true for industrial needs because purchasing managers index It remains below 50, indicating weak industrial demand.

trade economics

The future of packaging

Challenges facing the packaging industry aside, the rising trend in e-commerce activity represents an opportunity for SON. The global industrial packaging market is expected to touch $132.80 By 2032, this number will reach $1 billion, growing at a CAGR of 6.8% from 2022. This is primarily driven by rapidly expanding e-commerce activities and growing demand from the supply chain.Furthermore, sustainability is a significant trend in packaging, with estimates 70% of consumers are willing to pay more for sustainable packaging solutions. SON is committed and has the expertise to produce sustainable packaging that serves multiple end markets.With the rapid expansion of the online retail market, consumers are increasingly purchasing goods online, and this trend will continue 2028. This will translate into growing demand for corrugated packaging solutions. Not to mention, food and drink consumption on the go is on the rise. This will lead to growing demand for convenient and portable packaging, which will benefit SON’s flexible packaging division.

Acquisition of a leading Brazilian flexible packaging company

SON’s recently completed approximately $59.2 million in acquisitions non-appealable, an industry-leading flexible packaging company, in December 2023. It is a producer of single- and multi-layer materials, primarily used in flexible packaging. This strategic move will expand SON’s existing presence in Brazil, where its Sonoco Graffo facility is one of the largest converters of foil-based flexible packaging and one of the leading manufacturers of high-quality rotogravure printing and lamination. This strategic decision will expand its presence in Latin America and its flexible packaging capabilities to meet growing demand from new and existing consumers.Not to mention its $330 million acquisition RTS packaging The acquisition in September 2023 strengthens SON’s position in the production of 100% recycled fiber packaging for the wine, spirits, food and healthcare consumer markets. This enables SON to expand its operations in the United States, Mexico and South America.

relative valuation model

Author comments

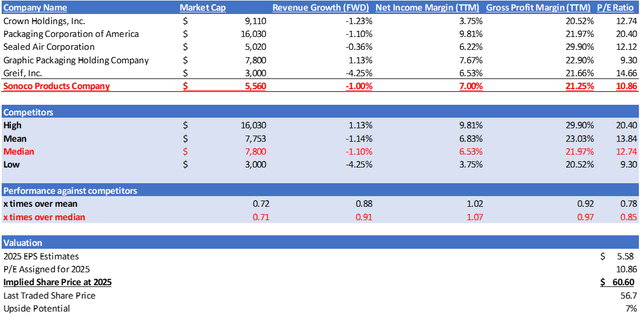

SON is engaged in the paper-plastic packaging products and materials industry. Among its competitors, most of FWD’s revenue growth has been negative as the industry has been facing headwinds from weak consumer demand and inflationary pressures. However, SON’s revenue growth of -1.00% was slightly lower than its peers’ median. In terms of profitability, SON’s gross profit margin is 21.25%, slightly lower than the median, but its net profit margin is higher at 7.00%, which is higher than the industry median.

Currently, SON’s forward price-to-earnings ratio is 10.86 times, which is lower than its peers’ median of 12.74 times. Given that its expected revenue growth and net profit are broadly in line with its peers, it should trade at its peers’ median P/E. However, given the headwinds for the industry, I think it is prudent to adopt a lower P/E ratio to remain conservative. Therefore, by applying 10.86x to consensus 2025 EPS estimates, I arrive at a price target of $60.60, which represents modest upside potential of 7%.

risk

The upside risks to my Hold rating relate to destocking and improving inflationary pressures. If destocking ends earlier than expected or inflation cools, it will create demand for the packaging industry. In this case, if SON reports better-than-expected results in the coming quarters, it could result in an upward revision to its expected revenue growth rate (which is currently negative). Although SON recently acquired RTS Packaging and Inapel, M&A activity has been limited amid the tough macro environment of high interest rates. With the market anticipating 3 to 4 rate cuts in 2024, we may expect larger transactions to occur and help support its negative revenue growth.

in conclusion

All in all, while revenue growth declined in 2023 due to low volumes, acquisitions helped mitigate the impact and the company demonstrated resilience through strong margins. SON faces destocking and inflationary pressures, but strategic pricing measures and the potential for input cost reductions offer promising prospects for margin improvement. In the long term, rapidly developing e-commerce activities and growing consumer preference for sustainable solutions provide SON with significant opportunities to consolidate its position in the industry. My relative valuation gives me a modest upside of 7%, but due to the lack of margin of safety, I currently recommend a Hold rating on SON.