ceramic graphics

Last weekend’s article detailed the S&P500’s (SPY) “inversion window” after testing the 5107-12 target.It’s easy to get carried away when the market stops doing exactly what you expected, and It was down 50 points, but two key factors were needed to confirm a reversal – a break above 5030-38, plus Friday’s close near the weekly range low – but neither happened.

Personally, I would prefer that we see a correction develop as I am underinvested and my trading style lends itself to a higher volatility environment. However, that doesn’t mean I fight this tendency every week – it’s tiring and often expensive. Identifying key levels and price action to monitor means I can buy against these levels, turn bearish if broken, or do nothing like last week.

this weekend The article will explore the outlook for March and the impact of the weekly Danish exhaustion signal. Various techniques will be applied across multiple timeframes in a top-down process, while also taking into account key market drivers. The purpose is to provide actionable guidance with directional bias, significance levels, and expectations for future price movements.

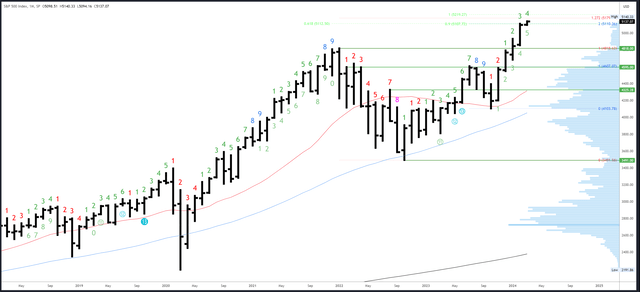

S&P 500 Monthly Index

The February bar closed near the monthly range high of 5096, and we have seen the expected continuation of the first trading day of March.

Now that new highs have been made this month, a bearish bar could easily form and fall back to the February range below 5111. Having said that, it needs to settle below that level, ideally much lower, which will obviously take some time.

In addition to the monthly charts, I am also watching the quarterly charts which are shaping up in a very bullish way. The fourth quarter was a huge pillar, closing at 4793 points, laying the foundation for the first quarter to break through the all-time high. The bar chart for Q1 captures this opportunity and could end strong (which obviously means March ends strong as well).

SPX Monthly (Trading View)

Fib clusters in the range 5107-112 elicited a small response. 5179 is the next Fibonacci extension (127% extension of the 2021-2022 decline). The next measured move is 5219 and the current bounce off the October 23 low will equal the October 22 to July 23 rally.

5096-5111 was important at the end of March, but not so important next week. 4818 is the first major level from the previous all-time high.

The wait for the next monthly Danish signal will be long. March is the 4th bar (possibly the 9th bar) in the new upside exhaustion count.

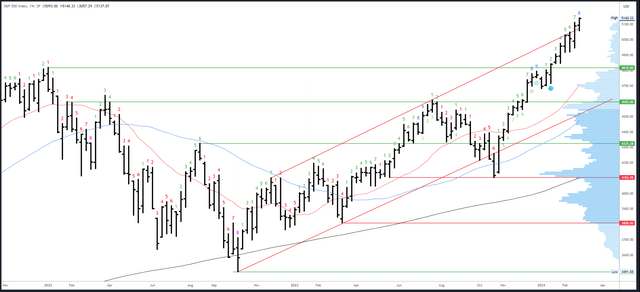

S&P 500 Index Weekly

This week has formed another bullish weekly pattern with higher lows, higher highs and higher closes. Seven of the eight bars rebounding from the January lows share the same characteristics.

The weekly channel high has now been broken more convincingly. In fact, I don’t take this too seriously – a breakout of the downtrend channel is more important – it just means there is no more potential resistance.

S&P X Weekly (Trading View)

The downside areas to watch are the same as last week. 5030-48 is the key to motivation. Below this, the 4918-20 double bottom is the next important area.

The upward Danish exhaustion count will occur next week on bar 9 (of 9). A reaction usually occurs in week 8 or 9, and this week’s new high should help the exhaustion signal play out. Warning – the last full signal caused the decline to last only one week!

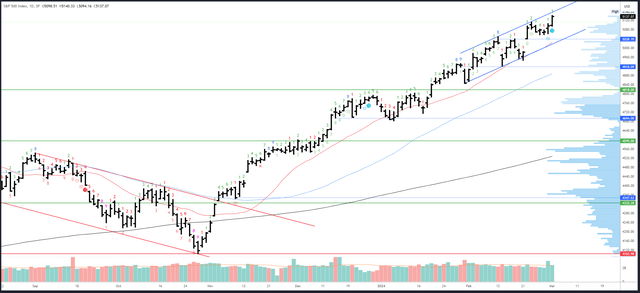

S&P 500 Daily Index

Thursday’s heavy volume and Friday’s breakout and strong close are noteworthy. A continuation is very likely early next week and 5105-111 should initially provide a dip.

S&P X Daily (Trading View)

The only resistance comes from Monday’s new channel high around 5160.

The first support level is 5105-111. Channel support is very close to the 20-day moving average. By the end of next week, both will rise from 5020 to 5050.

Denmark’s daily run-out couldn’t be completed next week, although a streak of 9-13 did complete it on Friday. I found these results to be mixed, but may be more reliable when combined with weekly exhaustion.

Driver/race

This week’s preliminary GDP growth was 3.2% from the previous quarter, which is very good, and the core PCE price index increased by 0.4% from the previous quarter. The economy and inflation are both heating up, and while rate cuts have been delayed, that’s clearly a good thing for stocks at the moment.

If the Fed switches back to a hawkish stance, perhaps these data will be more important. There are no signs of that so far, but I’m reminded again of last year, when a reacceleration of the economy triggered a series of rate hikes just when markets thought a pause was imminent. I think a repeat of 2024 is unlikely, but we may see a more hawkish message this week in Fed Chairman Powell’s two-day testimony on monetary policy.Will the Fed at some point consider Further tightening? Whether the data is good (no cuts needed) or bad (cuts will fix everything), they say nothing and let the stock market soar.

Powell’s testimony will take place on Wednesday and Thursday.

The main data release on Friday is the jobs report, which is likely to continue to show a very tight labor market. Whether this is a positive or negative for markets will depend on what, if anything, Powell thinks about the data.

Possible changes next week

Last weekend’s strong moves are expected to continue on Monday/Tuesday. 5105-111 should hold any initial decline, with Fibonacci extension targeting 5179. Powell’s testimony could cause some volatility, but unless he says the Fed is ready to tighten again (or at least keep rates higher for longer) based on the data, any reaction is likely to be irrelevant.

As always, there are Potential for reversal. Some weeks and arrangements have better odds than others, and since there will be a weekly exhaustion next week, the odds will be slightly higher. However, there is no point in fighting the trend unless something happens.

The daily channel and the 20-day moving average are the first good support areas. A break above these would be a red flag, but only Thursday/Friday weakness and a weekly close near 5030-38 would signal real danger to the uptrend.