Katherine Ziegler/DigitalVision via Getty Images

Introduction and thesis

Threshold UP (NASDAQ:TDUP) is a leading online thrift store and fashion resale platform founded in 2009. It operates in the second-hand fashion marketplace, allowing consumers to buy and sell high-quality, second-hand clothing, shoes and accessories.

TDUP has successfully achieved strong growth and brand development through innovation in the apparel industry, leveraging technology and changes in shopping behavior to increase traffic to its products. While this boosted the company’s revenue trajectory, its bottom-line financial developments were disappointing.

In our opinion, TDUP is not a business with attractive long-term returns. The industry has too many market players and could become normalized by a few monopolistic players, similar to the broader market industry (think eBay).Although we believe TDUP is well positioned, there are external factors such as maintaining marketing capabilities. We don’t want to spend money on gambling. We believe that investors who bet on TDUP becoming the “last man standing” did not receive adequate returns.

With less cash, heavy macroeconomic conditions and limited margin improvement, we advise investors to stay away.

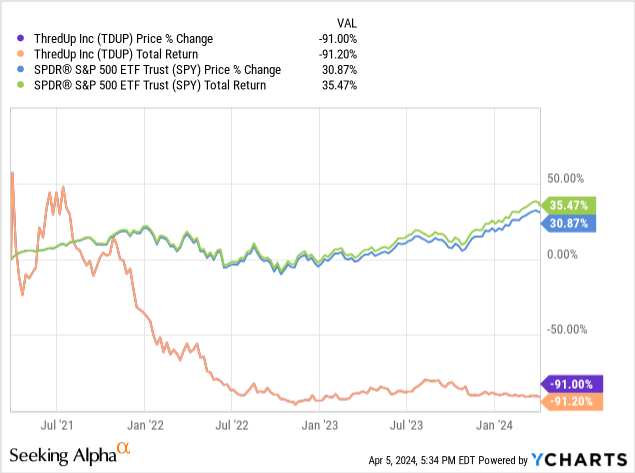

share price

TDUP’s share price performance has been disappointing, losing over 80% of its value in a short period of time. This reflects a broader market sell-off, particularly in discretionary industries, as well as poor financial developments.

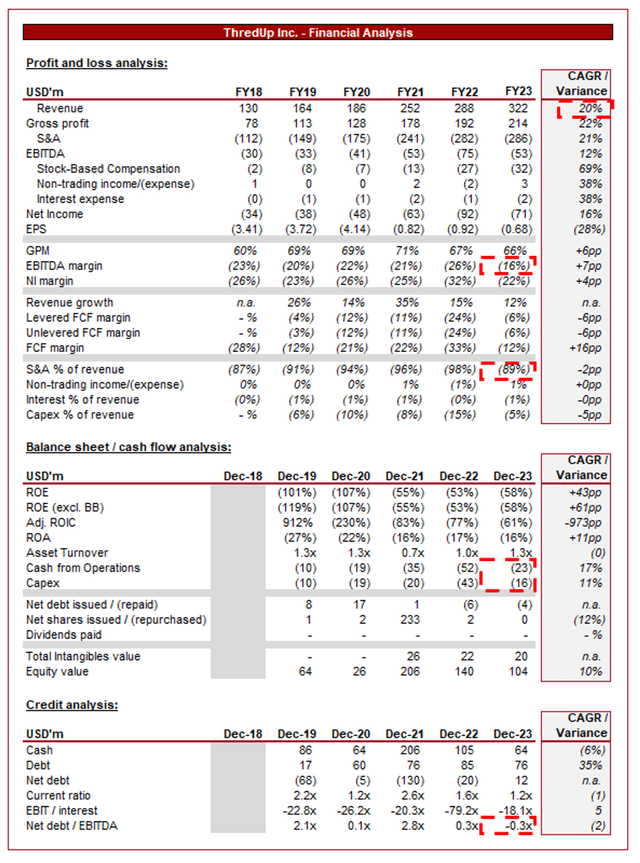

financial analysis

Capital IQ

The above describes the financial performance of TDUP.

Revenue and business factors

TDUP’s revenue has grown well over the past decade, with a compound annual growth rate of 20% in fiscal 2023. Despite this, profitability has not developed positively.

business model

Threading

TDUP operates as an online thrift store and resale marketplace specializing in the buying and selling of second-hand clothing and accessories. The model is in line with sustainability trends and caters to consumers looking for eco-friendly and affordable fashion options.

TDUP uses data analysis to select second-hand products and ensures quality and style levels through dynamic pricing. Part of this curation process involves a quality control team that evaluates and selects merchandise based on brand, condition, and current fashion trends.

TDUP’s inventory is primarily user-generated, as individuals can sell their frequently used clothing and accessories on the platform. This is a very important part of the industry because success requires creating network effects. Consumers want to shop where there is a variety of choices, and sellers want a marketplace where they can sell at attractive prices/times. We believe this will be a decisive differentiator in the coming years, as no peer has yet achieved a monopoly (in fashion). One of the reasons is the current inherent environment with so many participants.

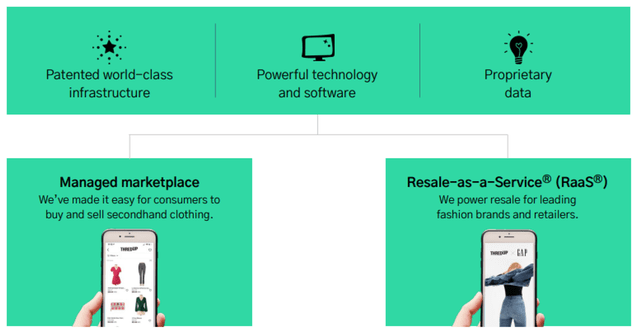

The company is expanding on the “resale-as-a-service” concept it created, essentially allowing fashion brands and retailers to create resale marketplaces and purchase inventory from customers. The company already counts H&M ( OTCPK:HNNMY ), Tommy Hilfiger ( PVH ) and J.Crew as clients.

Threading

TDUP simplifies the personal sales process by providing cleaning kits. Sellers can place unwanted clothing in these kits and TDUP takes care of the rest, including photographing, listing and shipping the items. This is yet another small factor that can help a company stand out from its peers and reduce friction, which is crucial in a growth industry.

We like the company’s efforts to maximize monetization and find new avenues for growth. The company discontinued the “Goody bag” product a few years ago, and while it failed, it was the innovation needed to succeed.

TDUP positions itself as a champion of sustainable fashion by promoting the reuse of clothing. The company emphasizes the environmental benefits of buying second-hand and contributes to reducing fashion waste. This is an important selling point, as well as a growing gap between rich and poor, both of which contribute to the continued growth of the second-hand market.

Threading

finance

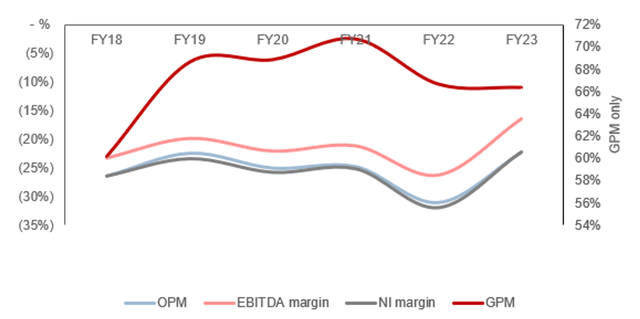

TDUP’s performance has slowed down recently, with revenue growth of (2.1)%, +4.4%, +8.2%, and +20.8% over the past four quarters. At the same time, profit margins also improved.

We believe the slowdown reflects the broader macroeconomic environment. As inflation and interest rates rise, consumers’ living costs continue to soar, but wages struggle to grow accordingly. This has led many people to reduce spending in order to protect their finances.

However, unlike many companies in this space, such as The RealReal (REAL), TDUP has managed to maintain overall positive growth. This reflects the products it sells and the market segments it targets. Since the company serves both high-end goods and savings services, it is well-positioned in a resilient market segment. Despite the difficult macro environment, consumers are arguably frugal when looking for discounts.

Capital IQ

TDUP’s margins barely grew and EBITDA-M improved by only about 7%, while revenue nearly tripled. The reason for this is difficult market dynamics.

Despite growing scale, gross margins have remained largely flat after fiscal 2019, indicating that the business’s unit economics are near their peak. Any further improvements can only come from tweaking its pricing structure, which could have unintended consequences.

With a gross profit margin of about 66%, there should be no problem for the company to make profits, but this is not the case. Since competition is fierce and this segment is growing, businesses need to invest heavily in marketing. TDUP currently spends 90% of its revenue on S&A expenses, and despite this, revenue is still slowing. The problem we see is that moats are extremely difficult to develop. Differentiation will come from the creation of network effects, essentially having a large number of buyers and sellers, making it an attractive market.

In fact, it’s hard to see how TDUP can make a profit. Since gross margins are quite tight, significant improvements can only be achieved at the operational level, and it’s difficult for us to achieve this without completely destroying growth and losing market share.

TDUP is currently burning cash, with an FCF margin of 15% during the LTM period. This reflects the significant investment it has made to grow the company, with the recent decline simply due to weaker capital spending. Fundamental issues with profitability will continue to keep free cash flow negative.

With approximately $48 million spent during the LTM period and a cash balance of $74 million, TDUP will need to raise debt or equity in the near future to stay afloat. Given that EBITDA parity cannot be achieved, shareholders may need to fund this.

Capital IQ

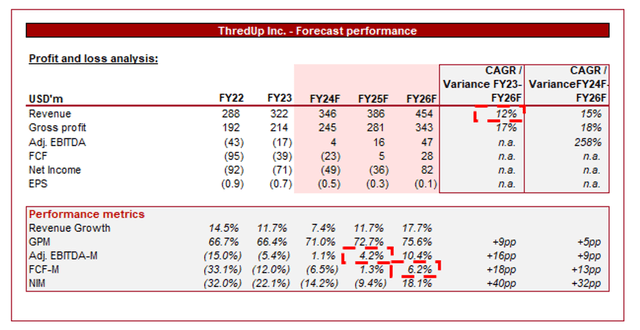

The above is Wall Street’s consensus for the next few years.

Analysts predict that the business will continue to grow, with a compound annual growth rate of 12% in fiscal 2025. Meanwhile, margins are expected to continue improving to adjusted levels. EBITDA is positive in FY24 and FCF is positive in FY25.

It’s rare for us to categorically disagree with an analyst, but right now we’re strongly skeptical. To drive margin improvement, growth spending essentially has to stop, which will inevitably lead to a revenue slowdown. It’s hard to see how the company can maintain anywhere near double-digit performance.

Furthermore, given the limited improvement historically, it’s hard to see how margins can decline so quickly, especially with EBITDA-M of (12.2)% in the most recent quarter.

Valuation

Capital IQ

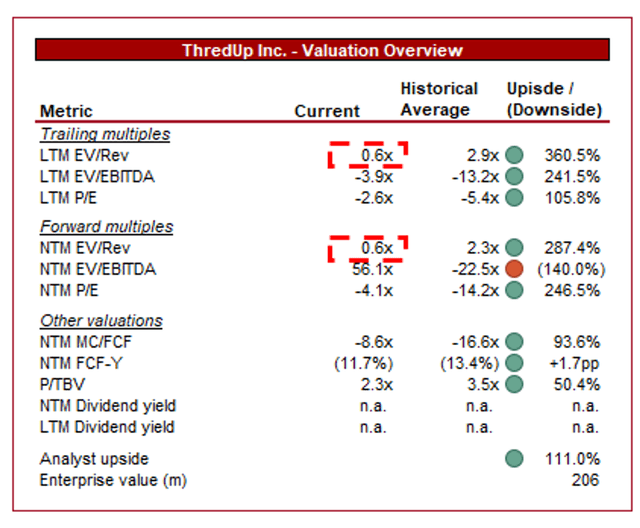

TDUP currently trades at 0.7x LTM revenue and 0.6x NTM revenue. This is a discount to the historical average.

With limited margin improvement and a weak growth trajectory, a discount to its historical average is certainly warranted.

Given the significant uncertainty associated with TDUP achieving profitability, we believe it must trade below 1x revenue, which is currently the case. We expect ~MSD to grow if costs are cut quickly and ~HSD to grow if costs are gradually reduced, suggesting a fairly rapid contraction in the multiple. So, despite being negative on the company, we don’t think it’s overvalued.

Key Risks of Our Paper

The risks of our current paper are:

- (top) Acquisition.

- (Upside) There is a growing interest in sustainable and affordable fashion.

- (Upside) Expansion into new markets and strategic partnerships.

- (Disadvantage) Counterfeit Scandal.

- (Cons) Fierce competition has not died down.

final thoughts

TDUP has a lot of potential. Management appears to be more aggressive than other teams we’ve looked at in this industry, and the stock trades at a deeper discount. The industry is highly competitive and we expect many peers (possibly TDUP) to exit over the next decade as the segment moves toward scale and consolidation.

However, we see no reason to take the risk on the company as it faces significant losses ahead, along with slower growth and minimal margin improvement.